As real estate investors & developers, we are always on the hunt for that next “diamond in the rough.” But what if the most valuable diamonds aren’t found? What if they’re made?

That’s the difference between a standard investor and an investor with a developer’s vision.

An investor with “Developer’s Vision” creates the Best Deal Possible.

It’s the ability to look at an empty lot, an outdated motel, or an underperforming property and see not just what is, but what could be. It’s a strategic foresight that goes far beyond blueprints and budgets; it’s about identifying an unmet need in the market and having the courage to build the solution.

This vision is the engine that creates value from the ground up. It’s how an investor moves from competing over the same scarce deals to creating an entirely new, high-demand asset class.

From Vision to a Niche Asset: The Large-Group STR

We explored this very concept in a recent episode of the REI Diamonds podcast with Andrew Llewellyn on the topic of Large-Group Short-Term Rental Investments.

This is a masterclass in developer’s vision.

Andrew doesn’t just buy a big house and hope a large group rents it. He dives deep into a specific market gap: the need for properties designed from the ground up to host large groups like family reunions, corporate retreats, and milestone celebrations.

This vision dictates every decision:

Acquisition: Finding land or properties that can be legally and physically transformed.

Design: Creating layouts with ample bedrooms, massive common areas, and unique, “wow-factor” amenities that groups can’t get anywhere else.

Operations: Building a management system that can handle the unique challenges and logistics of large-group turnovers.

By developing a product for a specific, underserved customer, Andrew’s vision allows him to create an asset that commands premium rates and faces far less competition than a standard 3-bed, 2-bath vacation rental. He isn’t just in the real estate business; he’s in the experience business.

Listen to the Full Episode

To get the full blueprint on how Andrew Llewellyn identifies these opportunities and executes his developer’s vision in the short-term rental market, you won’t want to miss this conversation.

Host Dan Breslin and Andrew Llewellyn discuss the unique and profitable real estate strategy of converting distressed, non-liquid commercial office buildings into highly liquid, cash-flowing residential-style boutique hotels designed for large group short term rentals. Llewellyn’s model works by acquiring property for the value of the “dirt” and transforming the asset. He capitalizes on Louisville’s favorable zoning and consistent demand, ensuring his properties are premium experiences rather than commodity rentals. Llewellyn views the operation as a “cash manufacturing machine,” optimizing efficiency and turnover using operational principles from books like Traction and The Goal.

Andrew Llewellyn & I Discuss Large Group Short Term Rental Investment:

The Strategic Advantage of Office- to Apartments Conversion (00:26:50-00:28:37)

Acquisition and Build Out Costs for the A12 Project (00:28:58-00:30:12)

Key Market Factors for the Duplicating the Strategy (00:31:16-00:37:09)

Future Pivot to Flex Space and Operational Strategy (00:40:04-00:46:26)

Relevant Episodes: (200+ Content Packed Interviews in Total)

Large Group Short Term Rental Investment With Andrew Llewellyn

Andrew Llewellyn, welcome to The REI Diamonds Show. How are you?

I’m great. Thanks for having me, Dan.

Getting Into Real Estate Through The Hospitality And Food Industry

For sure. Interesting topic and interesting asset class. I probably would label this maybe commercial real estate/short-term rental, which is intriguing. A lot of people are doing these mountain house short-term rentals. This is something new. Before we get into that topic, I have a question. Was it true that you were trying to open up a bakery business or something of that nature?

That’s some great research. Originally, we had purchased the building I’m in to be a wholesale bakery. Our city permitting council had other ideas for me in order to do the bakery. The cost shot up so much to the point where I was like, “I don’t think we can sell that many blueberry muffins to recoup that money.” During the tour when I bought the building, a buddy of mine had said, “You should Airbnb the whole place.” I thought it was a joke. It turns out that when I modeled it, we should Airbnb the whole place.

That’s pretty cool. What year was this?

This was 2021. It was still in that “Is the world going to melt down?” COVID era. I had two ice cream shops. We were running a food truck with that concept and a wholesale bakery out of the back of the ice cream shop. We needed to move the wholesale bakery. That’s how we got to this property. It got into real estate by mistake.

From a location stamping question, I’m in Chicago right now, and you are in?

Louisville, Kentucky.

It will be relevant to the rest of what we’re going to cover here. Why the food trucks? Was that a business that had a low barrier to entry? Was it family? This is an interesting start. We don’t hear it often on this show.

The food truck was a mobile concept of what we were running in the ice cream shops. Our twist on the ice cream shop was that we were doing the European Liège waffle. That’s a yeasted dough with pearls of sugar in it. I had the thought to add that product to the menu because you have one new product, one new piece of equipment, and you get a whole new menu. We were doing ice cream on top of these waffles. They were the same toppings as ice cream. From a production standpoint, it was super simple to set ourselves apart from the competition.

Is that cyclical? It’s not hot year-round in Louisville.

It’s very cyclical. It’s a warm-weather business only.

Is it still operating, or did you make the decision to close that down?

When the lease ran out, I decided to close it down because we were doing so well with our short-term rentals. After COVID, they printed so much money. The cost of a 15 or 16-year-old kid to scoop ice cream became expensive. Plus, they had to take tips. The food cost went crazy. All of a sudden, to make the right margin that we were making, we stopped being a snack or a treat. We were like a meal. We were having $40 checkout tickets for ice cream. That doesn’t fly. That’s not sustainable.

That’s wild. We have this hospitality food industry entry point into real estate. It feels like it was more of a business than an investment. I would like to ask about investment philosophy. That would be the set of rules or your thought process around investing. Do you have an investment strategy at this point, like an investment philosophy? If so, what would that be like in a sentence?

Our investment strategy is to buy a building for what the dirt is worth, something unwanted that has been on the market for a while, with some potential, and in a good location.

You then turn that around.

I guess the most familiar term to people would be the BRRRR model. Run the BRRRR model on a commercial building and turn it into a hospitality.

Getting A 10,000-Square-Foot Five Apartment Property

I believe this is your building. Is this the building you’re in now?

That’s the building I’m in now. I am in the basement of that building. Our guest showed up at the bachelor party. We typically do a full property buyout on the weekend. About 25 guys showed up three hours early before check-in time. I’m down here in the basement doing this show.

Here’s the interesting thing. For people who are not watching, you can check this out. What is this, Swepson?

You got that. This is the Swepson Guesthouse. This is 10,000 to 12,000 square feet. It’s a storefront with apartments above it. Those in Chicago and Philly know the deal with what this is. It’s 5,000 square feet per floor, give or take, maybe.

It’s about 3,300 a floor, 10,000 square feet total. We have apartments on every floor, including the storefront. We fogged that glass in and put apartments there. It’s pretty cool.

It’s an interesting loft-style construction layout here, 42 guests maybe, if you took the whole building. Is that right?

If you took the whole building and you packed it in, we can do 42 to 50, depending on how tight you want to pack it. Forty-two is a good place to stop.

This is spread across four or five apartment units total? What’s the layout?

It is across five apartment units, two on the first floor, two on the second, and then this cool, lofty space on the third floor. That winds up being the hangout space.

That’s a lofty spot. How many beds and baths per unit do you have in there?

It’s a mix. We have one four-bedroom unit. We have three three-bedroom units and one two-bedroom unit. It’s a bit of a mix.

How many bathrooms per?

There are two bathrooms per unit.

The details are important. I know you and I are looking at this, and you look at this every day because you’re working out there right now. For people reading, I’m trying to help paint the picture of what we have here. A 10,000-square-foot. I would call this a five Class-A apartments due to the construction, the detail, and design that we have here. What my mind goes to is, Airbnb is working right now. I’m sure it’s always going to work. You’re operating it very closely.

Even for somebody who’s going to make the loan on the property, co-invest, or own the property long term, if you don’t want to do the short-term rental thing at some point in the future, if the short-term rental thing becomes not a fad, or if people migrated away from it for some reason, the backup plan is you’re renting it out as an apartment building. You’re walking away with cashflows. Is that what you were thinking here?

When we decided to pivot from the bakery to this, it was like, “What’s plan B, C, and D if Airbnb doesn’t work out?” Plan B was, “We’ve got five great apartments in this building and a growing neighborhood. It should cover the note if the Airbnb doesn’t work out.” Luckily, it has worked out well.

One thing to highlight here, I have a property where I stay in the wintertime in Florida. I throw it on Airbnb. It offsets some of my expenses. It’s not a cashflow machine. It’s not a business I’m running. I don’t self-manage it. I’m not tweaking all the knobs and trying to make it push every last dollar the way that you can when you’re running the business. It was good the first year, and then 3, 4, 5, or I don’t know how many more, popped up in the same neighborhood.

One of the neighborhoods would allow it to happen. You could get a short-term rental there. It was legal. It was part of why I bought the house there. That’s why everyone else followed suit and moved in. Our creative property, 3,500 to 3,800 square feet, with the slides for the kids in the building and bunk beds. Suddenly, the neighbor down the street is putting in an outdoor basketball court and a pickleball court. They’ve gone Disneyland with it. There’s a ton of competition is where I’m getting at.

One of the niches in short-term rentals that you have taken advantage of here is that you can accommodate a small number of guests in one apartment unit. The thing that is hard to replicate is that somebody takes all five units and has the bachelor party, the wedding, and the corporate event. I look at a property like this, and I’m thinking to myself, “If I were going to have my family all together, we have a choice.”

We rent six or seven hotel rooms. It’s odd. We’re all eating down there in the public space. We find an interesting place like this. We take the whole building over, whether there are couples with kids, the grandparents, or what have you. You have this very unique place that you’ve created with a lot of flexibility and a high barrier to entry for someone else to come in here and compete with you.

With families, we find that they like that they can be together. There’s enough space to gather, have a meal, hang out, and be with one another. At the end of the night, as families do, you’re like, “I’m ready to get away. I want to go back to my unit. I’m good. I’ve had eight hours with you. That’s good. I want to go watch TV by myself.” You can do that. Families with kids who come here love that the kids are contained. The backyard’s fenced in, gated. They know where the kids are. The kids can run the whole building.

Large group short term rentals work best for families who want to gather for meals and hang out together in one common space.

It’s a great setup for families, large groups, and corporate retreats. We can see all our reasons that people stay with us up there. It’s a great place for everything. With the high barriers to entry, it is a big chunk of change to open one of these, and then to find a lender that believes that you can operate at this scale. That’s definitely a barrier to entry.

Breaking Down The Financial Aspect of The Property

Let’s run through what the numbers look like. What did this cost to buy? What did it cost to renovate? What is the high end of the rent if someone takes the whole building? What’s the low end of the rent? This thing is probably seasonal. You’re going to get more money at certain times of the year than the other.

We bought this in a questionably up-and-coming area during COVID. It was a big bet. It wasn’t for Airbnb like I talked about. We were like, “I hope the neighborhood turns around. It’ll be a great investment. We’ll have a cool property if the neighborhood turns around. If not, that’s okay. We’ll have a bakery. We’ll make it work.” We paid $980,000 for this building, which was not much. We spent about another $400,000 to renovate the first floor and furnish the place on one floor. When the property was purchased, it was this cool, lofty apartment on the third floor, and then two long-term tenants on the second floor. Their leases came up. They didn’t want to renew. That was another reason to push for this Airbnb project.

Did you also have to do some improvements on the other floors, or are they not quite like the other build-out?

They required, and I would put it in lipstick-on-a-pig category, a little bit of paint, a change in a couple of light fixtures, and a couple of bathroom vanities. It was nothing like the first floor, where we were putting in demising walls and plumbing. That was a complete gut and restart.

All in basis here, maybe 1.6 or 1.7, or something like that.

It is 1.5.

What are the rents looking like, high and low seasonally?

We’re typically running about $2,000 a night for the whole property. That works well for us. It produces plenty of cashflow. Depending on the month, it is $10,000 $15,000 in free cashflow.

That’s after the mortgage, the expenses, and the whole thing?

Yes. It’s a great deal.

Were you able to refinance all the cash out at the 1.5 basis?

We were. I’ll speak to that quickly. When we decided all of a sudden, we were doing real estate instead of ice cream and food service, it became clear that I needed to take a couple of courses. I found a couple of online courses. I don’t remember what they were, but I learned about cap rate, refinancing, and NOI. I got up to speed on everything. By the time we had started construction, I had an idea of what the process needed to be and how to execute on that.

You have the most accidental real estate beginning. There are people who have the accidental thing, but usually, it’s like, “I read Rich Dad Poor Dad. I found out about rental houses, and then I went out and did X, Y, Z to get into real estate.” You’re like, “We’re here making these ice cream pies. We couldn’t do it, so we decided that this would work,” then it did. On the website here, you have your newsletter. Sign up here. Keep in touch. That’s good, if anyone wants to check that out.

Understanding How A Residential-Style Boutique Hotel Works

That site that I looked at here is SwepsonGuesthouse.com. You could check out those photos for yourself or check out our video on YouTube. We have this first very interesting mini hotel/experience/oversized Airbnb asset class. I don’t know if a boutique hotel is how it fits. How would you define this? You watched a couple of courses on commercial real estate, so clearly, you are an expert by now. How would you define the asset class?

It sits in no man’s land. Let’s take the perspective of banks. If you go to a bank that loans on Airbnb, they say, “No, it’s a hotel. We don’t do that.” If you go to banks that do hotels, they say, “It walks like a duck. It’s an Airbnb. We don’t do that.” It’s in between. The term that we’ve come up with is residential-style boutique hotel. That’s the best way we figured out how to clearly describe it to people and be articulate with it.

I’ll probably agree. You’re pretty hands-on. You’re in the basement and probably talk to those guests who are upstairs.

My favorite part of the job is meeting the guests, finding out where they’re from, finding out why they came to Louisville, and giving them a tour of the property. That’s a highlight.

It makes sense. The investor stack, were you independently wealthy, and then you built this project because you had enough money to do it? What was it like? How did you get it done from the beginning? It was $980,000 to accidentally do a real estate deal. You’re like, “It was a good deal.” That’s almost $1 million. That’s a big swing.

I had the ice cream shops. We were doing well with that. My dad was my business partner. He was silent off to the side. I called him. I was like, “This bakery thing, we’ve got to get this out of the back of the ice cream shop. We need a new space.” Dad had been in business for a while. He was like, “I’m tired of seeing you pay rent to somebody else. Let’s go find something to buy, and I’ll help you. You can get it stabilized. We can figure out the bank thing in a little bit. I can’t stand seeing you pay any more rent.” Dad’s tired of seeing us pay rent. A buddy of mine knows someone in his real estate office who owns this building. She was trying to offload it quickly.

Dad stepped in and said, “We’ll deal with the banks later. I’ll help you purchase it.” Dad purchased it with me and with the idea that it would be a bakery. That was very helpful. When we got to the Airbnb part, by the time we got there, I had taken the real estate courses. At the time, it didn’t feel so whimsical and like “This is such an accident.” It felt more like, “I’ve got a million-dollar problem on my hands. We’ve got to dig in. We have to solve this.” It’s how it felt. In that process and taking those courses, I understood then, “If we do this, we add the value of the renovation. Dad can get his money back out. We can move along. We can keep going.”

These buildings are hard products to make work. We’re doing deals all over the country, probably 1,800 since 2020, and 1,000-plus before that. Any time we get these mixed-use storefronts and apartments above them, it’s a very limited buyer pool. The tenant pool is also limited. You’ve got to be in a prime real estate location to get Starbucks or some national tenant in there, and then suddenly, the building looks like a no-brainer.

Ninety-eight percent of this product is not national tenant type locations, Class A locations, where you’re going to be able to get that. You’re stuck dealing with the local ice cream guy who leaves at the end of his lease. The product doesn’t have a lot of buyers. It is viewed as highly risky, the storefront with a couple of apartments above it. I can imagine the fire lit under your ass as you were sitting there with this million-dollar building and no more bakery plan. Did the neighborhood end up swinging up a little bit since then? What happened in the market there?

The neighborhood thankfully continues to grow. We’ve had a couple of other entrepreneurs in the neighborhood come in. There’s a guy in the neighborhood. It’s a QOZ. It’s a qualified opportunity zone. That’s actually helpful for bringing in the neighborhood and getting it to rise. The city has been putting a lot of dollars and promotion behind getting people to come to the neighborhood and be entrepreneurs here. Across the street, two girls opened a fancy wine bar and a coffee shop. That has been great. We’ve got a carpet store next to us, a wedding shop, restaurants, and a brewery. It continues to grow and grow.

Acquisition And Build Out Costs For The A12 Project

Some of that, you were part of the trailblazing pioneer. Your dad’s faith is admirable in taking the step in that direction, as is the case for a lot of real estate investors who take the plunge into these areas on the upswing. We covered that case study pretty well in detail. Let’s switch gears here a little bit. You had mentioned a new project.

It is called A-12.

The A-12 project is probably bigger than this. I couldn’t find much info or photos online. You’re going to have to paint a picture all on your own using words.

We’ve been very purposeful about not having that out there yet. We want to have a good launch with it, trying to tease it as much as we can. The picture is that we are three blocks away from Whiskey Row in downtown Louisville. This property that I currently sit in, geographically, is about 2 or 3 miles away, so they’re generally pretty close. They’re about five minutes apart driving, but it is in the prime bourbon tourism location that you want to be. It’s 18,000 square feet of a 1970s warehouse that was then converted to 1990s office space.

When I purchased that building, it had an adult daycare on the first floor that was on a month-to-month verbal lease at half the market rate and an ACT high school kids’ test-taking prep on the second floor, also on a month-to-month verbal lease. That property had been on the market for almost 500 days. Nobody wanted it. I walked in, and I was like, “This is a huge problem. I don’t know if I can take this one on.”

Just out of curiosity, I called a real estate lawyer that I knew. I was like, “How much if I have to go all the way and evict these guys?” He gave me the number. I was like, “That’s not that bad,” considering the size of the project that we would have to do. I was like, “Let’s try it out. It’s 18,000 square feet. We’ll end up with 32 bedrooms down there. We’ll run essentially the same exact model that we run at the Swepson of large groups that need a place to stay together and then want some cool hangout space to be able to actually gather, not in a public hotel lobby.

Will those 32 bedrooms be laid out in ten units or something like that? What would that look like?

That’ll be laid out in eight four-bedroom units and then two annex units in the basement.

It’s so great because, even from a retirement perspective in commercial real estate, we deal a lot with owners of businesses who are 75, 80, or 85 and are still running their business. A lot of times, we have an offering on a 9,000-square-foot warehouse. The guys are closing down this odd niche, little stamping business. The exit on that is not very liquid. We have to take risks. It’s the same thing you’re dealing with. We have to get it at a good price. There aren’t a lot of buyers out there.

There are some buyers out there. I even liken this to the Swepson house. Had you bought it, run the bakery in there, and then run that until you were 75 years old, you turn around and sell it. You’re selling this odd mixed-use thing with the storefronts. That’s not a lot of buyers out there. There is not a lot of great exit out there, whereas the model that you have, you can run this for assuming the market holds up for 10, 20, 30, 40, or 50 years, however long. If a day comes and you want to retire, you have a highly liquid asset in a logically built-out with large-unit apartment building.

Barring big negative population growth or something like that, aside from single-family houses, apartment buildings are the most liquid asset that I’ve dealt with out of all the asset classes. It’s simple. The banks know it. It’s easy for people to understand. It’s like the apartment they lived in, so they can relate to it. You have a huge buyer pool compared to many other businesses running in their own or operated locations that then have to exit their unique, not-so-liquid, hard-to-figure-out property. It is exactly what you bought here in 18,000 square feet of office space, in today’s environment.

The people we bought it from are a legacy family in Louisville. They have plenty of money. The brother-in-law was tasked with managing these tenants. He was like, “I have a family office that I operate. This is a thorn in my side.” We offered him around $50 a square foot for it above ground. That was off the ground. It was $11,800. We paid $1.18 million for it. It’s got 25 parking spots downtown in the central business district.

You even have a lot there.

We looked at it. We’re like, “What would somebody pay for this lot? That’s probably what we’ll pay for it.” We picked up the headache of the tenants.

That project, if I had to guess, is probably going to run somewhere around $1.2 million to $1.5 million to build.

Yes, a little bit more, with the furniture and the plumbing.

It makes sense. Is it wide open lofts right now? There’s the frame and everything.

It is completely gutted. It’s just four walls, a white box, essentially. I’ve had guys in there for a month, gutting the ’90s office space.

What a great asset, though. Once it’s all done, it’s all modern plumbing. It’s the newest wiring with brand new insulation wrapped around it. You have probably 100 years of usable life out of what goes in there. In some of my old apartment buildings, which I got rid of, there was the cloth wiring. It’s a never-ending repair pit. This is a great example of office building adaptive reuse, or the mixed-use thing. It’s tough, and it’s a cool way to reuse that space.

Key Market Factors For The Duplicating The Strategy

I guess this would work in some areas of Chicago, but it doesn’t work everywhere. If people are reading, they know of some building, and they want to duplicate the strategy in another city, what are a handful of things they would look for and say, “Yes, it would work in this location, this neighborhood”? What are the things that drive this large group gathering event space that you’re running?

Here’s the first thing I would look at. Can you run a residential hotel, a boutique hotel thing that we’re doing here? Can you run that in a commercial building? I know you can go down to Atlanta. No chance you’ll be able to do that down there. You’re going to have to get rezoned, that whole process. I wouldn’t say we have a lack of zoning laws, but they’re not as strict as in some places. “Can you do it?” is the first question, with the zoning. The second question is, do you have the neighborhoods surrounding you to support it? Every time you go to a hotel, you’ve got a coffee shop. You’ve got a place to get breakfast. It’s got a gym and a workout room. Does the neighborhood have those amenities that you’re not going to put in the building? You don’t want to end up on an island by yourself.

Make sure the neighborhood around your hotel has various amenities available that you will not put in the building itself

What about demand in the area? We can’t have this in a high-crime area, in an area of town where things don’t work. We have the coffee shop. We have the gym. Maybe we even have a bunch of restaurants around there. In Louisville, you guys have the Kentucky Derby. You got this bourbon culture thing going.

I always tell people, Louisville Tourism, the organization that promotes tourism and gets events to come to Louisville, the whole city is riding on their back. We’ve got the Kentucky Derby. We’ve got two giant music festivals. Two weekends in a row, they attracted over 100,000 people, back-to-back weekends. That’s huge for a city like Louisville that has a million people total. We have one of the larger convention centers and a tertiary market. Also, we have a giant fairgrounds. They keep those things booked. We’ll do obscure events year-round, like a farm and machinery show. The power company has those trucks with the buckets. They’ll have that convention. We have the Rabbit Breeders of America convention here.

I know a guy who used to attend that.

It’s obscure events after obscure events that are bringing tens of thousands of people to Louisville. Here’s the last piece that drives traffic for us specifically. Louisville is fairly easy to get to because it is central to the United States. There are a lot of remote teams out there that are trying to find a place to get together. We’re finding corporate retreats that need to get people from all around the US together in one place. Louisville is central on the map.

You have to be in a location where you can potentially have a corporate retreat. Ideally, you have some tourism functions there, maybe sports teams. You guys have the Kentucky Derby, but those same tourism things are going to be part of the draw for things like bachelor parties and bachelorette parties. Family reunions probably even need some semblance of a tourism draw.

You don’t want to be out in the middle of a small town in America, where there’s no population, no airport, and barely a highway exit. This is not going to work there. There’s probably a spectrum of rural near-zero population, near-zero traffic to New York City or downtown Chicago. A little further back on that is maybe the Louisville market. Somewhere up at that other end of that population, that tourism thing, this strategy works. It’ll be left to the eye of the beholder to figure out where that is.

I did a small case study with a mentor of mine. He said, “Why don’t you go to Nashville next? It’s the bachelorette version of Las Vegas on the East Coast, and plenty of traffic. You can get it to work.” We looked at it. The problem is that the real estate costs twice as much there. There are so many investors there that the rental rate is half. The math doesn’t work on paper. You have to find that right balance for the market and the aging of the market, too.

Before opening a rental property in a certain location, make sure to strike the right balance between what works on paper and what works on the market.

Is there a strategy for underwriting the rent? How did you determine that Nashville was a pass and that the rates were half of where you’re at?

They have a lot of class B or class C inventory of large units. There are guys down there building zero-lot-line houses and multi-story condos, and doing large group stays. They’re not unique. They’re commodity-type things.

How are you going to stand out?

They are not three times the price cooler to the commodity guy.

A lot of them are going to be commodity guys when it boils down to the end. That’s part of the issue I’ve always had with the short-term rentals. I was bullish on it when I bought my own vacation house in Florida. I’m like, “This is great. The projections look great.” Year one was great. That was probably 2023 or something, then the bubble popped. It seemed like all that printed money that you were talking about earlier cycled its way back through to its rightful owners.

It is the government.

It is probably those who figured out the game of money who are tuning in to this show. Certainly, all of us have some of that in our pockets and net worse here at this point. It’s that competition thing. Airbnb, several years ago, or whenever it first came out, you could put these somewhat dated places to stay, and people would do that. You couldn’t get away with that. I remember 2017 or 2018, I had an Airbnb. Mine was the dated apartment unit. It’s booked. It did okay. It was in a decent enough neighborhood that was trending, probably similar to where your project is located, translated into the city of Chicago, but then everyone else was competing me away. They were renovating units. They weren’t even cool, but they were a fresh renovation.

What happened in Florida, we were on the front end of the design and coolness with my property. That got trumped exponentially two or three more times by the next units that came on. You got a good thing going. I don’t know how duplicable it would be. I’d probably caution the audience to make sure you’ve dialed in the business model and tested the market and all of your assumptions before you pull the trigger on a $980,000 purchase for the asset no one else wants.

We were lucky to have the first floor and, at the time, the second floor. We were getting a little bit of cashflow from there. It was covering the interest, so that worked.

Future Pivot To Flex Space And Operational Strategy

It sounded like a perfect deal, especially for deal number one here. We have A-12 cooking and being developed. What’s the future looking like for you? What is the goal in 12, 18, or 24 months, or in 5 years? What goals do you have? What vision do you have for the future? It seems like you’re working towards something.

We’ll probably stay in the real estate game. I like the side of real estate that we’re in. You can put some business acumen into it. You can set yourself apart from the competition and do something a little different to get a premium price per square foot, if you want to put it in real estate terms. I don’t know if we’ll actually do any more short-term rentals, to your point. There might be a city where we could do it, but the economics of getting there and running it probably don’t work.

We’re here in Louisville. This is where we live, and it works well, but getting on a plane and spending a day or two getting there is not a passive game. For the audience, I’d be cautious about that as well. We might start looking into some higher-end flex space. I have a couple of friends who are doing that in different cities. Listening to them, the business acumen that they’re applying to it, and helping those smaller, newer, unsophisticated business owners grow their business and have a nice space to run it out of seems interesting.

I think that flex is having its moment. There’s certainly a place for that as an asset class. You’re absolutely right. The inability to scale what you’re doing is what I suspect would happen. I probably would have worried for you if you’re like, “We’re going to have 62 of these things in every city, including Anchorage, Alaska.” Maybe you can do it. I have a friend who had a similar product to what you have here in Savannah, Georgia. It was great for a while, but he didn’t live there.

He lived in Boston. It was the flights and the back and forth. Eventually, the management got tired of it. He sold it. He exited. Ironically, that guy is doing pretty much all flex space now and loving it. He’s doing some scaled-up deals, but in the interim, if I were in the basement, that was my office, I’m working there, and you don’t mind it, great business model. Let’s run this thing.

I don’t think the scalability is there. It’s so hands-on, which is fine. We’re getting paid well for what we’re doing. I don’t see it scaling with the amount of capital required to build one of these. Unless you’ve got multiple family offices in your pocket that are super bullish about large-scale Airbnbs, you’re probably not going to be able to scale it nationwide.

It makes sense. Have you gotten any repeat bookings yet? Are there any people who come for the same week, year after year, and you can inch up the rates on them?

We’ve got a couple of those guys, a couple of church groups that come every year, corporate retreats, and sales teams that bring customers in. They spend money, take them on the bourbon trail, and have a great time. We’re getting more and more of those. Our Thanksgiving guest is actually a family. That’ll be their second time with us.

It seems like the endgame for one of these other vacation homes that I have my eye on. It’s a summer town in New Jersey. I’m like, “I don’t know. Short season, egregious prices out there, but I like going out there. I’d like to stay for a month or six weeks before I head to Florida.” Some of the allure is that it is the same family who is coming. That’s their week. The second week of July, they take their vacation. They’re going to do that for ten years.

It seems like this great end goal, where you have your property. It’s like January, and the same people are there. It’s a twelve-week season or something. Maybe nine or ten of those weeks, it is the same people. As soon as they’re done with that vacation, they book for the following year. It’s something to repeat native subscription revenue out of real estate at the high end when you’re dealing with these group luxury rentals that we have here.

We’re trying to push more and more recurring revenue from past guests. Part of our business is milestone events. Let’s hope you don’t have two bachelor parties. Guys, don’t turn 50 twice. That recurring thing for us is a little difficult. We definitely need to work on it.

What other things do you think are relevant that I may have forgotten to ask about?

We hit all the main real estate side investment points about this business, the way we look at properties, buying them for the dirt, and building them back up.

Andrew’s Book Recommendations

There are a couple of quick questions here as we close and wrap up. Book recommendations. I’m interested to hear one or two books that you found impactful as you started on this real estate journey. I’m expecting to be different than a lot of the guests who showed up because your path is.

Let me give you probably three, the most impactful for this business. Gino Wickman’s Traction is amazing. FranklinCovey’s The 4 Disciplines of Execution is about leading measures. Eli Goldratt’s The Goal is for looking at this as a cash manufacturing machine and sending cleaners through here efficiently to get the place clean quickly and turned back over.

Mentorship will be effective if you take the time to have an actual conversation. You should know when to keep quiet and not ask too many questions.

Those are some interesting ones. Two out of the three, I have not heard of or considered before.

Which two are those?

Covey and Goldratt’s. Traction is making its rounds. We hear a lot of that. A lot of us have gotten a lot of value out of Traction, 100% worthwhile, but the other two are interesting. I have to get those ordered.

Those are good.

Get In Touch With Andrew

Where do you want readers to go? I know you mentioned a couple of websites early in the show, but where should readers go if they want to get more information?

If they want to get more information about staying with us, it is SuperStaysSTR.com. I love to help you plan your bourbon trail trip, corporate retreat, bachelor party, or fiftieth birthday party. If you want to follow the renovation down there at A-12 from the office to a boutique hotel, and probably eight months to a year is what it’s going to take us, you can follow me on all of socials @IAmAndrewLlewellyn.

Take The Time To Have A Real Conversation

My final question, I ask all the guests, what is the kindest thing anyone has done for you, Andrew?

It is taking the time to have a conversation with me and let me ask questions, not telling me, “You’re asking too many questions. Be quiet.” It is mentorship.

Ditto. I have a couple of pages of notes. It was a great topic and a cool business model. I appreciate your time, Andrew, coming on the show.

Andrew Llewellyn, CEO/Founder of Super Stays STR, is a real estate entrepreneur in Louisville, Kentucky, who specializes converting non-liquid commercial buildings into highly liquid mini-boutique hotels for large groups.

His strategy thrives on a strong local demand and is highly optimized using business systems.

When I was younger and less experienced, I held the naive belief that real estate always increased in value. Even now, I could point to hundreds of deals that have appreciated over the past decade without any capital improvements. However, with a bit more experience and a few gray hairs, I now see the truth: some properties are worth *less* 5-10 years later, regardless of the capital invested.

The real estate market doesn’t care how much you’ve invested in your property. It’s worth only what a buyer is willing to pay. In commercial real estate, that value is driven by the rent a property can command. That’s the ceiling.

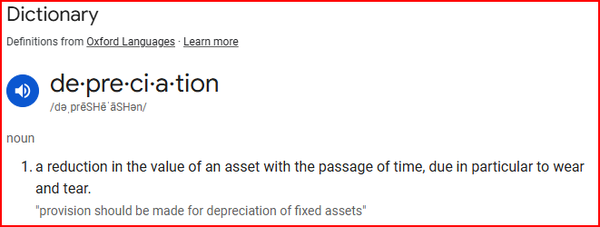

Many of us real estate investors joyously danced at tax time this year, grateful for the lowered tax bill from depreciation. However, we should look closely at the definition of “depreciation”: a reduction in the value of an asset over time, due in particular to wear and tear.

Hmmm, that sounds a lot like “worth less,” doesn’t it?

In commercial real estate, this concept is often alarmingly accurate. Retail leasing, for example, frequently comes with two huge upfront expenses: leasing commissions and a tenant improvement (TI) allowance. If that tenant fails, you don’t recoup those costs—you pay them all over again for the next one. This is just one example of how wear and tear erodes your value. Let’s look at a few more.

National Retail Fast Food – Single Tenant Net Lease

Ever wonder why so many national brands like Starbucks lease their locations? Because they know their format will evolve over a 5, 10, or 20-year period. Starbucks adding and removing drive-thrus or changing its “third place” experience are prime examples. Rather than getting stuck with an obsolete building and losing money on a sale, they leave that risk with the landlord.

We recently made an offer on a closed Burger King. The seller had paid around $2.5 million when a corporate lease was in place. The tenant paid for three years, then went bankrupt, leaving a dark shell. Vacant, the property now needs a $500k refresh and a $200k leasing commission, or perhaps a total demolition and rebuild for over $1 million. The value of this property today is maybe $600k. The tenant’s failure erased nearly $2 million in value.

The Hotel & Motel Industry

Our team has recently seen a scourge of old motel and hotel properties coming across our desk. Many sellers bought them within the last decade, but the market has changed. A new generation of superior hotel products has made the old, roadside models obsolete. Sure, these properties may still produce some income, but nowhere near enough to justify the original purchase price paid by the current owner. The numbers just don’t work.

There is a trend of investors converting these outmoded buildings into affordable housing, but the purchase prices must be exceptionally low to make the numbers work.

On the other hand, many newer hotels are built with kitchens and distinct bedrooms. This smart design is optimal for future-proofing; in 20-30 years, when the hotel concept is obsolete, the units can be easily rented out as long-term apartments.

Of Course, Office Buildings

No article on value destruction would be complete without a nod to office buildings. The office sector has been overbuilt several times throughout history. Even the World Trade Center, completed in 1973, didn’t reach full occupancy until the mid-to-late 1990s, just a few years before its destruction.

Today, many office buildings in prime locations are being sold for little more than their land value, destined to be torn down or converted to multifamily housing. That said, I’ve started to see a turnaround and am bullish on the office sector’s comeback. I notice a significantly higher impact from businesses with a strong in-office culture compared to those that are 100% remote.

This ties back to my general bullishness on cities. Office buildings offer the same concentration of intelligence you find in vibrant urban centers, where ideas can be developed quickly. This process is painfully slow over Zoom meetings with dozens of faces on a screen, where people awkwardly articulate ideas and the audio cuts out during spirited discussions. In person, when the best ideas are forming, everyone is present, has a voice, and can feel the energy of creation.

Why I Buy Value-Add Real Estate

The commercial deals I pursue require a strategic repositioning to become functional and profitable again. You can’t just raise rents on an underperforming property; you have to fundamentally improve it to *deserve* those higher rents. Vacancy doesn’t fill itself, even after a full renovation. A skilled leasing broker has to work the phones, find the right tenant, and earn their commission by securing a durable income stream—the lease—which is what truly creates value.

All of that said, I do buy the types of deals mentioned below, but the price must match the quality of the asset and its current, in-place income stream.

Have anything like this for sale? I am Buying:

(I Need a $4M-$8M purchase to close by year end.)

Industrial & Commercial Property, 10K sq. ft. – 250K sq. ft.

Mobile Home Communities (50 pad minimum)

Well located Retail Development Sites

Residential MFR & SFR

Located anywhere in the U.S.

Value Add Required-There MUST be a path to push the value

Ideally long term rented asset with below market rents

Host Dan Breslin and Natalie Cloutier discuss her unique Build, Rent, Refinance, and Repeat (BRRRR 2.0) strategy for real estate investing. Leveraging her architectural technology background, Natalie Cloutier explains how she scaled a portfolio of high-quality, dense, small multi-family new builds starting with zero capital. The conversation details the practical aspects of her business, including maximizing bedrooms for higher rents and managing significant development risks, such as unexpected municipal fees. Ultimately, the discussion highlights how strategic building and densification offer a superior, capital-recycling approach compared to buying older rental stock.

This Episode is Also Sponsored by the Lending Home. Lending Home Offers Reliable & Low Cost Fix & Flip Loans with Interest Rates as Low as 9.25%. Buy & Hold Loans Offered Even Lower. Get a FREE IPad when you Close Your First Deal by Registering Now at http://REILineOfCredit.com

Natalie & I Discuss Build-to-Rent Development:

BRRRR 2.0 (00:01:30-00:01:55)

Mitigating Development Risk (00:15:18- 00:18:42)

Tenant Vetting & Operations (00:31:38- 00:37:28)

The Sabbatical (00:37:23- 00:24:16)

Relevant Episodes: (200+ Content Packed Interviews in Total)

I am great. Thank you so much for inviting me on. I’m very excited to be here.

I’m glad you came. When I saw the booking come through and do a little preliminary research. I was like, “This is an interesting one. We haven’t explored this topic and not a lot of people are doing it or talking about it.” We’re going to be talking about the build-to-rent for the folks reading. There’s a lot of institutional money doing that. That’s what I thought when I saw the topic, “It’s the institutional thing.” It’s not that. The readers will be surprised. Before we jump into that, though. One of the other interesting fun facts here. I’m recording from Chicago and you’re recording from?

Canada in Ottawa, so the capital of Canada.

I have some friends doing some development in Winnipeg now with a 30 or 40 or 50-story building or something like that with the university. I think in a partnership, it’s a cool project to watch these guys bring out of the ground.

That’s awesome. I don’t do that.

Understanding Natalie’s BRRR 2.0 Strategy

I wouldn’t be little or talk down. The things you’re doing are very interesting and they’re relevant for what we have for the audience. Let’s start with the investment philosophy. If you had to distill your investment philosophy, your strategy down to like a single sentence. What would that be?

I’ve been using the BRRRR 2.0. If your audience is familiar with the BRRRR strategy that Brenda Turner coined, the buy, renovate, refinance, and repeat or whatever. I might be missing R in there. I do the build, rent, refinance, and repeat. It’s basically the same strategy and what’s cool with it is that you can recycle capital endlessly to grow your portfolio and scale it to whatever amount of units you want to do.

How Natalie Started Out With Zero Capital

For the reader who hasn’t figured it out and didn’t do the research. Would you mind telling us the origin evolution story? Maybe use those photos on the wall behind you.

For those who are looking on YouTube, I have a couple pictures behind me of the houses we build. My mother-in-law likes to paint our projects. These are the first starter projects that we started with. What’s great with the strategy is that anybody can start. We started at nineteen years old with $0. We had no money. We had a basic entry-level salary and graduated from college. We built our own house, which is the greenhouse here. We still live in it. I’m sitting in it and we house hacked, which I didn’t know was a thing back in the day.

We added a basement apartment to help supplement the income because, as I said, we had crappy salaries starting out. We started with $0. We started by buying a basement unit condo right out of college just because that was the only thing we could afford. We bought it with the CMHC first-time buyer loan. Which for you guys in the states, it’s similar to an FHA loan. You go in with a low down payment but you get a higher interest rate in exchange. We were just excited that we were approved for a mortgage but then going in, you realize the interest rate was about 6%. Plus the condo fees were adding up.

As soon as we walked in, they were scheduled to go up. You don’t have a yard and a garage, and you’re in a basement. A few months in, we were very unhappy. My parents sat us down and they’re like, “I’m going to get you in on the little family secret.” They told us about how you can build your own house for $0 dollars down as long as you do some labor work. You get in there and you do some labor yourself to save the money. That’s what we did.

You can build your own house for $0 as long as you do some labor work yourself.

We built our house. Long story short, we got a basement apartment, lived for a fraction of the mortgage, and then we got a HELOC. We found this very cheap lot local to us. It was a problem that nobody wanted to buy but we have a background and we studied architectural technology. That’s where my husband and I met. We’re not architects but we’re like the CAS ad monkeys, if you will, or did the draftsman. We said, “With our background, maybe we can make something happen with this lot.”

We bought it with the HELOC and we built a little single-family home that we eventually converted into a duplex a couple of years down the road and we kept going. We’re like, “This could be a recipe for a business.” Eventually, after a couple years we realize, “This is investing.” This is an investment strategy. We went in blindly.

Dealing With Fear, Hesitation, And Doubts In Real Estate

You’re getting ready to build the first house. You found a piece of land. Do you remember what was going through your mind as far as the fears or the hesitations as you were considering doing it? Maybe there were any because the family was like, “This is easy. We’ve done him a hundred times. No big thing.”

There’s so much fear. I remember the first day when the excavation equipment was coming on site to come and clear the land. My husband threw up in the bushes because he was so nervous. We were not confident in any way possible. When I told my husband about this, the strategy that my mom talked to me about. I was trying to convince him and we got into this huge fight because he’s like, “I’m not doing that. I’m not taking risks.” He came from a family that never took this risk.

After we did one, he was the one pressuring me to do the next ones. It’s funny how that works. There was a lot of fear and a lot of doubt, but it definitely helped that we had my parents in our corner. They had it built. They built four houses in four years before they had my sister and I, which was like 30 years or 20 years prior to this house. They had experienced but times changed.

They were nervous about it too a little bit, but they had a little built my sister’s house years before. I don’t remember how many years ago. They were helping us through it. We had that guidance, but we knew that it was something we wanted to do because we were just unhappy being in a basement condo. We wanted to do more, so we did it anyway. I’m glad we did.

It’s very interesting. The architectural background, having a mom with experience pushing you in this direction and a husband. What’s the husband’s name?

Rob.

Rob’s over there throwing up in the bushes. I bet the readers can relate. I know I certainly can, even though I’m like 1,800 deals closed and tons of construction and still, I feel not fear but certain anxiety. It’s like, we came through 2020 through 2023 with the inflation that happened, and a lot of very sophisticated investors, companies, and people who’ve been doing the business for 10 years, 15 years, 20 years, and 25 years got jammed up. Some to the point of bankruptcy from the cost overruns when lumber went from, I don’t know what the numbers were, but it was like a 10X cost on just the lumber. Let alone the labor and every other thing you’re going to need. You can’t stop halfway through.

You got to keep going.

Was there a moment in the build that was the same one? The excavator shows Rob’s up chucking in the bushes. Was there another moment where maybe halfway through and maybe it’s like being out on a rope bridge and your past appointed a return or was that it when they were like doing the excavation?

I think that was it because once you get the ball rolling and you get working, for us anyway. Especially when you’re doing the actual physical work. You just get into this work mode, survival mode, and we’re in it. You got to finish it. There’s no turning back now. You just get into that grinding and keep going. Once we had to let go over excavator. It wasn’t working well. We had to hire another one. Early on, we learned the ropes of managing trades, finding the good ones and the importance of all that. It had a stressful moment but this was many years ago already. It’s getting a little blurry. We’ve lived some scary moments since then and all of our other builds. That I can say.

The Challenges Of Mitigating Development Risks

What’s the toughest trade, maybe that you have the most problems hiring and finding or maybe just one of the toughest challenges you faced over that ten-year building cycle out of all these properties that might be like a pitfall for other people to look out for?

That’s like two separate questions. First for the trade. One of the traits that we had the most problems finding was a good plumber because plumbing is tricky. You’ve always got working components with the water and stuff. That’s the first issue like floods and leaks. I think we went through three or four, maybe five plumbers. Now, we finally have a good one, but we’re about to take a break for a year and sit on our assets for a little while. It sucks when you finally have built your team up for ten years. Plumbing was probably the trickiest one because then you have to do service calls during management and then you want to make sure that they follow through on that.

In terms of probably the hardship that we’ve lived. One of the reasons why we’re taking a break for a year, we’re going to do a little bit of soul rejuvenation after that. There’s a lot of things going across the board. Not just in Canada and Ontario, but across the board. There’s new bills in California and Wisconsin that came up to incentivize affordable housing, where anything to make affordable housing help builders cut the red tape and just make the process faster and make it more affordable for people to get in and find rentals.

In 2023, they did that. The province passed a bill, where you could add a secondary dwelling unit onto existing zoning. I’m going to make it easy to understand. For example, if you had a zoning where you were allowed to do a single-family home. You were allowed to add a basement apartment, let’s just say. Now this new bill allows you to add another apartment on top of that already allowed apartment. If you have like this project here, for the people looking. This used to be a duplex. There was no third floor.

We ripped off the roof. We set it on the front lawn. Built up a third unit, and then we put the roof back on when that bill passed into doing three. We doubled the income of that property. That was one of the things we did with that bill. The other thing we could do is if you were allowed to do a semi-detached and then you could add basement units. With this bill, you could add other units on top making it into a sixplex, which saves you the development charges. You only paid development charges on the two main dwelling units. You don’t pay them on the secondary apartments.

That was huge for us because in Ontario, the development charges are like $40,000 for the main unit. You’re spending a lot of money. It would have been in 140,000 permits on a sixplex that we instead paid a fraction of that. The problem we had or the hardship we lived in was that because this was all very new and this was the province’s goals and not the municipality’s goals. The municipality is influenced by the province, by the Upper State to follow these goals. If they don’t want to follow it, they don’t have to.

They’re the ones missing out on these development charges. If you’re going in to build a sixplex that they would have otherwise had like $140,000 of income from that permit. Now, they’re only getting $60,000. They’re not very happy about it. What happened was because we were the first ones in applying for a sixplex in the area. They let it go with the pre-consultation. They were all okay with it, but then when it came time to release the permit, they had some time to do some internal policy changes. They decided to charge us the full amount. We were very unhappy about that because that skewed our numbers completely.

The price from the start, the numbers from the start didn’t make sense. We had a long battle with the city. We got lawyers involved. We got the province’s ministry and the leader of the city involved. Anyways, we had to fight it out and they kept saying, “No, we don’t care.” Eventually, we went for an appeal in front of the city council and that’s where we won. We won our case and we got credited at least $40,000 back which was better than nothing.

That took a toll on us because it was unexpected. It’s something that your audience could maybe learn from. You have to make sure that you’ve got all of these initial consultations with the municipalities in writing, in Black and White, that you are allowed to do this and that means something until you get your permit. There can be a significant amount of time between the time that you do your initial consultations and your studies to the time that you’re ready to pick up your permit. Sorry, that was a long story, but I feel like it’s worth mentioning.

Make sure to make initial consultations with municipalities in writing when securing real estate deals.

We love stories like this, Natalie. I appreciate the granular detail here. It’s extremely relevant and it highlights the development risk. In a moment, we’re going to take a look at some of the projects. For anyone reading, it’s probably worth going and checking out the video to see the quality of the new construction. It fills in the rest of the story.

It probably also justifies the aggravation and the risk to have this quality class A asset when it’s all said and done. Even if you had to overpay for it by $100,000. If you asked for a 5 or 10 years from now, that is going to be a superior product with higher rental rates than the existing stuff you could have bought that’s 30, 40, 50, or 70 in some of the areas where we invest 100 to 150 years old.

You get a class A tenant from the start, too, which is great.

For the new construction.

That’s what I mean. Sorry.

We ran into that. We have a development project. We’re going to go in for like 7 or 8 units and get that approved. We have a developer who’s going to take the project from us assuming the approvals come. The neighborhood filed with the historic society to try to get it labeled as a historic house so that we couldn’t tear that down. Historic society is like, “This person uses this as a weapon. It’s a pretty common tactic or technique. We don’t see any historical value here.”

My fingers are crossed. Maybe by the time this is live, we’ve gotten our good news and we’re at least one more step into the entitlement process toward getting it done. These are the things that you run into on a development. It’s very common for a $40,000 or $50,000 or six-figure unexpected expense before you even get your permits and that’s where the risk comes in. There’s a certain amount of value that a developer can bring to the market. When they bring a lot that’s entitled and has a permit issued and it’s basically what we call shovel-ready in the industry. It’s a separate topic for another day.

At the same time, it’s worth mentioning because there is risk involved. If you do your due diligence correctly and you go in with the right conditions before even going solid on your offer. You can mitigate that risk. There’s always a way, but especially when you’re doing larger development, then it gets riskier because there’s more studies involved. There’s more contingencies you have to plan for. If you stick to small multifamily, there’s a way to make it a lot less risky.

If you do your due diligence in real estate correctly and set the right conditions before even going solid on your offer, you can manage and mitigate development risks.

The Price Tag You Should Be Preparing For

What’s the price tag on that? We’re doing some large 100-lot subdivisions and our price tag is about $200,000 to $300,000 at least. Sometimes $400,000 in soft costs, meaning the engineering, the architecture to figure out if we’re going to get the answer from the municipality of, “Yes, you can build,” and we have a project or not. What is that line item for you? You have a lot. You’re going to build 2, 3, or 4 units there, and you’re in due diligence on your contract. Before you lose your earnest money and you got to perform, you have to pay how much to get the answer, whether or not it’s a project you can go forward with?

First of all, that’s why we don’t do development the way that you were explaining it, like the 100 lot development. We don’t do that, especially because of that. It’s very high risk. You need a lot of capital. You need to fund it for a long time. We don’t do it because of that. We stick to infill projects, where the lot and the services are there. Basically, you take property in an urban area. You’ll tear down a house maybe, and then you’ll rebuild and take advantage of the zoning loopholes where you can identify a little bit more than just a single-family home.

Let’s say before you even lift your conditions on your offer and you go firm on your offer. You probably only need a couple thousand because you just need to do maybe a soil test. The conditions that I usually tell people to do is to do a soil test. Make sure your soil makes sense and you’re ready if you need a bigger foundation or whatever to support that soil. You need a pre-consultation with the municipality to make sure that they are in favor of the project you want to do. You want to be clear and upfront with them and you need your financing conditions.

For the financing, you might need to hire a designer to get at least a preliminary done. You don’t have to have the full set of plans done, but you want to make sure that what you want to build fits on the lot. If you want to do a sixplex, fourplex or a triplex, you want to make sure that it fits within that fill project, that lot. You might have to pay a couple of thousand for that initial design or probably not. It’s probably just a few dollars.

For us, we do the designs in-house because we started architecture. I do the designs myself. It’s just that soil test of $350 that we pay for and that’s it. It depends on what project you want to do, how big you want to go and what you need for your conditions. If you’re doing something bigger than a sixplex, then it usually falls into commercial lending. You might need environmental studies. That’s a different ballgame, too. You might still be able to stay conditional on your offer until you can at least raise like phase one of that environmental study. That might be a few more thousand dollars, but we’ve never had to do that yet. We try to stick to small multifamily because the numbers just work.

In the US, the limit would be four. Five units up in the US is commercial financing. Four and under fits the owner-occupant far easier.

It’s the same thing here. It’s just that when you go for six or more, you’re still commercial lending but that’s when the lender might ask for environmental studies. As a fiveplex or sixplex, you might still not need them yet. It just depends on the lender and their specific requirements for the number of units you’re doing.

A Deeper Look At Natalie’s Real Estate Projects

We would hit that with five units. You would fall into that book. Let’s take a look at some of these projects. We’ll treat this like a case study. This is what I thought was cool. It’s the Instagram page. Nice brick facade. We’re looking at a duplex.

It’s a triplex that we just finished building.

You have a two-door entry on the front.

One, you have to go down a couple steps on the side of the building and that gets you into the basement walkout.

It’s a great-looking building.

Those are like larger three-bedroom and three-bath units. We have a four-bedroom in that triplex. Our biggest unit yet.

A four-bedroom?

A four-bedroom and three-bath at the top unit.

What does it cost to build this? It’s Canadian dollars, but we could do the calculation.

This one, we did with a joint venture partner. It was our first time with the joint venture. We’re doing a sixplex with him as well. There’s more cash involved because we’re making sure that all the duties and responsibilities are separate. He takes care of money management. We take care of the actual construction. We’re paying ourselves a rate for each of those. We’re at about $750,000, I have to say. I don’t know the numbers. What is that in America, probably about $550,000?

That’s great.

That’s pretty good. It is valued at about a million.

Is that based on cashflow typically on an appraisal or comparable sales?

They’ll do all three approaches on your appraisal. They’ll take the cost approach. The income approach and the comparison approach, and then they’ll give you a fair market value with those through approaches. It depends on how much weight they want to put on each. In my book that I wrote, I talked about and explained the appraisal process in detail. It’s about the same in the states. The process is very similar for new construction because I spoke to a couple of people in the states. They’ll just take a general amount based on those three approaches.

In the City of Philadelphia, we have an office just outside of Philadelphia. A lot of the audience are from that region, but they’ve had a pro development support, I guess, subsidy. When you build a new building there, you get a ten-year tax abatement. It didn’t matter if it was in the higher-end area, the lower-end area, etc. The lots are small. We’re talking like a 600 square foot lot or 750 square foot lot. Tiny lots, but you could buy them very cheap in areas that were lower income, build a six-unit building as long as it was a corner lot, and then do like public housing. Get an income-based appraisal because there were no six flat comparable sales to get all their cash back out.

His strategy, the guy I know who was doing this, was not to sell any of them. Only keep recycling to cash the same way that you did. I love this build, particularly. A lot of long-term readers probably have heard me say this before, but it’s all about beds and bass when you’re buying a rental property. It’s like, if you’re going to house hack, go out, get the most bedrooms and most bass that you can because you’re going to come in.

The ability to rent to a family as opposed to a one single person or a couple, if this was a one-bedroom, one-bath unit or three-bedroom and three-bath. Now, you maybe got two or three roommates, if you want to accept that, who can afford a higher rent. Maybe you have a family or a couple and two or three children who will probably make that a home and stick around a lot longer than someone who’s a little more transient in the one-bedroom unit.

Over time, the higher rent as it increases and inflation occurs. It just turns out to be a much bigger number that moves the needle. For me, how much dollar and rent can I get for each roof, each unit? The maintenance costs there, if I had have ten units to make that certain rent versus maybe three units to make the same rent. Now, I only have maintenance calls on three units and not ten. I love the three-bed strategy. You put like a classic A product out there that just has no competition.

That’s the goal. A lot of people will stick to two bedrooms because it is easier to manage a tenant that way. When we’re talking Airbnb’s or short-term rentals, then that’s where people maximize bedrooms, typically. For long-term rentals, a lot of the local builders here will stick to two bedrooms also because sometimes that’s what fits the most on a lot. When I’m designing the space, I try to maximize it as much as I can because, as you said, it gives you a broader shot at the market.

It’s less competition. It’s cool that you’re the designer. You’re the one who sat down and made these decisions.

I designed the whole footprint and the outside and all that. I have a lot of fun with it. That’s the part I like doing the most. This one is a six plex that we did. This is the one we had the whole fun with the city council where they owed us $40,000. This one is a sixplex and I loved it. This one is more of an inner rural area. We had to do a septic field for that one. A little bit lower rents, but still three bedrooms and one bath.

What is the rent there?

These are $1965 and we include the internet for $40. It’s more like $1,925 and then for $40 more, they get the internet included. We just put the Elon Musk dish at the top there.

It’s literally that rural?

Yes, exactly. Bell services stop right before this building. This is something that was a hiccup that we learned only after during the build. We thought we weren’t going to get internet access at this building and we were freaking. We’re like, “People need the internet more than the water these days. What are we going to do?” Bell was like, “It’s there. It’s just that, to get it, it stops right before your driveway. To get it to you, it’ll be like $30,000.” We’re like, “Screw you, Bell.” We got Starlink instead and we got a tech guy to wire the units. We put one dish on the roof, and it feeds all six units.

This is from April 28th, the picture that we’re looking at. Do you have six tenants now living in this building?

I do.

Have you had any complaints about the Wi-Fi?

There was one day that they said it was a little slow but I think it’s because it was like a Sunday. Everybody was using it. It just happened. Our tech guy said, “If everybody’s at home using it at once,” which is usually rare. Most people are out and about. Not all six or there at once. We have people doing night shifts and stuff. It doesn’t always happen that way but it only happened once. We had one complaint once from one tenant. I didn’t hear from the other five.

They probably did deal with it. We live in a condo building. There’s 450 units in our building. It’s like a city, but the internet is often slow and that’s why I was wondering. Maybe I’ll have to get a Starlink dish and put it on the balcony railing out here or something.

We love it. My husband’s parents have a cottage. Very rural. It’s like a nomad’s land. They don’t even pay taxes. It’s in the middle of the woods and they never had internet for their 50 years of owning that cottage. Now, they finally got to the Starlink dish and they’re all excited. They’re texting us from the cottage.

How Natalie’s Strategy Evolved For The Past Several Years

Very cool. A couple of things here, class A tenants. We talked about the investment philosophy, the buy-to-rent, and all that. Has that evolved at all? It sounds like you guys just build to rent right from the very beginning. I’m curious if there’s any evolution around your strategy in the way that you invest over the past years.

We grew our business. We grew our team. When we started, my husband and I were doing work around the clock. We started with a forward focus and we were strapping lumber on top of the focus on the roof and that thing. We were working 40 to 50 hours a week and then working nights and weekends on our builds. We didn’t have much starting off as a couple. Eventually, now we have a full-grown business.

There were some hiccups obviously with COVID, the high prices, the lumber skyrocketing and the interest rates skyrocketing. We just always stuck to our core value of staying under leverage. That’s the most important thing that you can do. It’s to remain under leverage throughout your journey because when crap like this happens like interest rates skyrocketing, COVID and all that nonsense. We kept our heads above water. We had positive cash flow in each of our properties. There’s not one.

For a lot of Americans, they don’t know this but in Canada, we have to renew our interest rate every 3 to 5 years. You can lock your rate for a year, 2 years, 3 years, or 4 years, but never more than five. Some lenders will do ten but I’ve never lived that. You guys are very lucky that you can lock in a rate for 25-30 years. That blows my mind. The first time I heard that, I was like, “What?” We don’t do that. There’s a lot of renewal rates in 2023 when the interest rates were spiking or had spiked.

People were going from 3% rates to 6%. A lot of people were cashflow negative and barely holding on to their investment properties. There’s a lot of sales, too. We managed to stay afloat in all of them. We had a little less cash flow for a few of them. When we finished a build, we tried to stay within the 70% loan to racial value. A lot of builders will try to maximize the loan so that they can pull out as much cash as possible.

We usually try to stay moderate with that and we’ll pull out maybe $40,000 or $50,000 if we can. Sometimes less than that and then we recycle that into the next project. We make sure that we’re below 80% as much as possible. We didn’t change our perception that much of the build-to-rent. The industry changes around us but because we stuck to being more risk averted or mitigating that risk. It helped us a lot. I don’t know if that answers your question, though. Is that what you were asking?

That’s spot-on. How does it evolve? Maybe you did it by default in the beginning, but there is a temptation for investors to milk the cash cow and go to the bank to take the money out. I watched a lot of people go belly up in 2007, ‘08, ‘09, ‘10, and ‘11 and that was the strategy. I remember this one guy. He said, “I had a closing.” We went out to dinner and it was a nice restaurant. He’s popping champagne and everything. I said, “Tell me about the closing. We did this and this. We did a refinance and got $90,000.” I’m like, “This is not a celebration. You didn’t make a profit. It’s not sold in the books here. You owe that $90,000.”

You have to make sure you can pay that back with high rents and interest rates.

Dealing With Tenant Vetting And Operations

Being on the lower leverage side is a critical and important piece. Class A tenants, was it a deliberate choice? Did it happen by accident? Maybe some advice on people who are dealing with class C and maybe highlighting a few of the differences if you wouldn’t mind.

I luckily do not have a lot of experience with class C. I’m very happy about that. I can’t compare the two. I’ve had some tenants that gave us problems. I have a list of those but that just came with experience of not vetting correctly. In the beginning, sometimes we’re just nervous building our first properties. The first person who came up and it was ready to rent. We would do like the soft check, but we’re like, “They’re just ready to rent. We know we’ll be able to cover the mortgage. We’re good. Let’s do it.” We had issues with those tenants specifically, but that was in the first few years.

The biggest piece of advice I can give people and I tell this to everybody now when I’m doing coaching calls or whatever. I tell them to make sure you take the emotions out of the equation at all times. There is no room for that in business. You have to be backed up by data and numbers. When you’re vetting someone, like if you can’t find a good tenant that passes all of your criteria. You’re better off keeping the place empty for a month or two until you find that right person, especially in Ontario. Where it’s impossible to get rid of a bad tenant. The tenant board is not on your side.

If you cannot find a good tenant for your property who passes your criteria, you are better off keeping the place empty for a month or two.

You want to make sure that you’re not getting tenants where they’ll cause you issues because I’ve lived it and it’s not fun. Vetting as much as possible. Calling references is probably more important than just checking documents. Calling references and asking the tough questions and speaking on the phone with them. Not just getting a letter because anybody can type up a letter. You want to catch the person in their life. If you can do that, if you can vet someone and then create systems.