Case Study 90,000 Sq. Ft. Industrial – Office in Atlanta, GA MSA

All week long we’ve been dealing with Operating Agreement Details, waterfall profit distribution discussions, and sending financial docs over to the Life Insurance Company doing our loan. This will slow down once we close DD and simply await the closing. Here are the Details:

90,000 sq. ft. (actually a bit larger)

8.7% cap rate on current income

National & Regional Tenants with 3+ yrs on Lease

10% Vacancy – to add to marginal value

$17,000,000 purchase price

$8,100,000 Capital Raise projecting 8% distributions beginning Day 31 (fully subscribed)

Why are We Buying this Deal?

This deal is projecting an 8-9% yield to Limited Partners paid monthly, beginning on day 31. If you’ve ever invested in syndications, you know this is special. It is very rare that distributions begin immediately. Normally they begin in the 1-3 year range-after a value add plan has been executed. This deal is special.

This deal is located in the Atlanta MSA, in one of the Northern suburbs. An 8.7% cap rate is a solid deal in a market like this. But, if this deal is so good:

Why the Seller is Selling?

This deal is 3 buildings, each about 30,000 sq. ft. One of these buildings is office space. The tenant was just acquired by a national company and resigned a 3 year lease. The risk is that the tenant leaves at the end of Year 3 when the National decides the location is redundant. 30,000 sq. ft. of Office Vacancy is the risk in this deal.

The Value Add – Redevelop the Office

If the office tenant leaves, we will redevelop the office building into 3 spaces of Industrial Small Bay-a red hot asset class right now. This deal only works because above the drop ceilings in the office building there is plenty of height to reconfigure the use. However, this is not cheap. A redevelopment of this size may run $500,000 or more. We’ve raised this capital up front-so Limited Partners will not receive a capital call in Year 3 if the tenant vacates.

Delusional Optimism – The Home Run Potential

If the office tenant leaves, the distributions will slow down as the space is vacant & during the time of the redevelopment project. It might be a tough year or so while that occurs.

However, if the office tenant stays, and we either give NO TI money, or even a few hundred thousand dollars, this deal becomes a home run. We have already budgeted for dealing with either of these scenarios going into the deal.

I wrote this article on how Delusional Optimism plays into my decision on whether or not to do a deal.

The Office Building

How to Invest Alongside Diamond Equity

Here at Diamond Equity, we have two main types of investments:

Syndication Deals: 5-10 year hold periods. 18%-25% IRR

Most of these deals mentioned above are funded through a few phone calls & texts without ever being sent out to this email list (like today’s featured Atlanta Industrial – Office deal – $8.1M fully subscribed).

If you want to be added to my personal short list to place capital in our deals, reply to this email with the estimated amount to deploy, your cell number, & two times & dates that work this coming week for a quick phone call.

On the other hand, if you prefer to just see the investment opportunities which make it to the email list, you can sign up here.

I asked a successful real estate developer this question over a lunch early in my career. He sat back & thought a moment before answering with one word: “Vision.”

What is a Developer’s Vision?

I’d define a Developer’s Vision is seeing something that can be done with a property that no one else believes is possible within the confines of maintaining a profit. Often, there is additional investment to create a superior project to anything found in comparable sales-with the faith that your project will command a premium.

Developer’s Vision in House Flipping

House flippers with Developer’s Vision often buy houses from us in rough condition and are much more creative in their construction phase than I would imagine myself. Small one story house receives a 2nd story addition. The façade is transformed by adding a larger porch or reconfigured entry way. Both require additional investment compared to a standard renovation project where no major alterations are made.

Note that Developer’s Vision is different than simply fixing up a house and selling it. If you look at comparable sales and match the renovation to what the market has already accepted, this is not really a visionary activity. It may be the safest route to a profit, but no new, grand “Vision” was executed.

Executing a Developer’s Vision is risky because there are no comps proving the value. You build a 2nd story addition and create a 4,200 sq. ft. house in a highly rated school district where no other sold homes exist with more than the 2,100 sq. ft. home you modified within a half mile radius to “prove” the market’s willingness to accept such a home. Risky.

However, this same inability to “prove” value offers the opportunity to price much higher than you could if there were already another property just like it. This is where Developer’s Vision pays off big-assuming you’re right and the market agreed. This is how new price records can be achieved.

Here’s an example where a small additional investment, adding a small porch and “address shutter” feature transformed the curb appeal:

The interior of this home was also impeccably designed, and I’d say with optimal Developer’s Vision. (Developer credit RESolutions Team, LLC)Photos

Managing the Risk -vs- Reward

In conclusion, for anyone reading who has limited experience in flipping houses, I’d suggest ALWAYS matching the renovation quality found in nearby comparable sales. You might implement Developer’s Vision at a small scale, as in the front porch example above to test your design skill. Before executing a larger Developer’s Vision, such as a large addition or any project exceeding $10,000, I’d plan to have at least 20 successful projects under my belt.

Danny Newberry, founder of Vail Commercial, joins Daniel Breslin to discuss Newberry’s evolution in real estate investing. He shares the key lessons he learned in his journey from residential properties to commercial real estate, including the benefits of triple net leases and the importance of strategic management. Danny also covers market insights, cash flow considerations, and strategies for finding value in commercial investments. Tune in to this conversation full of valuable information about making the transition to commercial real estate or looking to enhance their investment strategy.

This Episode is Also Sponsored by the Lending Home. Lending Home Offers Reliable & Low Cost Fix & Flip Loans with Interest Rates as Low as 9.25%. Buy & Hold Loans Offered Even Lower. Get a FREE IPad when you Close Your First Deal by Registering Now athttp://REILineOfCredit.com

Dan Newberry & I Discuss Investing in Commercial Real Estate:

Transitioning to Commercial Real Estate (00:01:39)

Danny discusses his journey from residential to commercial real estate, highlighting the gravitational pull many investors feel toward larger deals.

The Impact of “Rich Dad Poor Dad” (00:02:24)

He reflects on how reading Rich Dad Poor Dad at a young age sparked his interest in real estate investing.

First Investment Experience (00:14:30)

Danny shares his experience buying a sixplex during college and how it opened his eyes to the potential of real estate.

Challenges of Managing Multifamily Properties (00:21:22)

He talks about the overwhelming management intensity in multifamily properties and the cash flow challenges that often arise.

Advantages of Triple Net Leases (00:25:40)

Danny explains the benefits of triple net lease agreements, where tenants cover taxes, insurance, and maintenance, reducing the landlord’s responsibilities.

Evolution of Real Estate Investing (00:27:00)

He describes the progression from single-family homes to multifamily and finally to commercial real estate, highlighting the learning curve involved.

Market Insights and Timing (00:42:35)

Danny discusses how changes in the interest rate market influenced his investment strategy and decision-making processes.

Importance of a Strong Tenant Profile (00:39:50)

He emphasizes the significance of securing tenants with solid financials to ensure consistent cash flow.

Focus on Smaller Commercial Spaces (00:40:23)

He expresses his preference for small bay industrial and neighborhood shopping centers, noting their quick leasing times and lower management intensity compared to larger assets.

Long-Term Holding Philosophy (00:46:22)

Danny shares wisdom about the importance of holding quality assets long-term and understanding market dynamics to maximize investment returns.

Relevant Episodes: (200+ Content Packed Interviews in Total)

Investing In Commercial Real Estate With Danny Newberry

Danny Newberry, welcome to the show. How are you doing?

I’m fabulous, Dan. Thanks for having me.

Danny Newberry’s Journey To Commercial Real Estate

We’re going to get into investing in commercial real estate withVail Commercial Founder, Danny Newberry. He and I have been friends, business partners for the past several years. He’s got an interesting journey to the place where his business is now. We are going to dive into a lot of that. Why don’t we start? A lot of the people on in my network and the audience of the show, we have a lot of house flipping. We have a lot of real estate agents. We have commercial real estate investors.

I’m going out on a limb, there’s a lot of people reading who would love to make the transition as they see people closing commercial deals, hear about refinances. There’s just this gravitational pull, if you will, from larger deals to the starting place for a lot of investors in residential real estate. Would you mind going through the thought process and the moments in time as you shifted your gears into commercial real estate?

Absolutely. Yeah. I’ll take you back from the beginning. Essentially, when I was in high school, my grandmother actually gave me the book Rich Dad Poor Dad. I remember reading it and it just struck a chord. I was like, “This is awesome.” I’ve been looking for something. I had probably already started a half a dozen small time businesses for a high schooler, like candy machine vending business, kitten smuggling from Utah to California and a handful of other ones that were semi profitable. Ultimately, when I read that book, it just really hit me that I think I can create what I want with real estate.

At that time, I was really going down the multifamily path. The first building I ever bought was a vacant six-plex. It was my first year of college, and I put it under contract for $155,000. I ended up closing it with my best friend’s dad, who was a hard money lender. He gave me the $155,000 plus $30,000 to fix it up because it was completely vacant at the time. Over the summer, I had fixed it up, filled it up, and it appraised for over $300,000. I’m like, “Why would I go back to school for a degree? I don’t have to make less money than I made on my first real estate deal.” That was the eye-opener for me that I’m like, “This stuff is real. It works. I want to go into this full-time.”

I quit college and ended up going after a lot of different assets in Southern Utah. I decided to move to Las Vegas because I was like, “I need to go to one of these hard-hit markets, either Southern Florida Phoenix or Vegas.” I lived like two hours from Vegas, so I’m like, “This makes the most sense.” I ended up moving out there and bought a ton of these 4-plexes and 10-plexes and smaller apartment communities. What I quickly realized was the management intensity was overwhelming and my cashflow was not there. I was buying these things super cheap. I will say it probably didn’t help that I wouldn’t even consider them Class C or Class D locations.

They were more like war zone properties in Vegas and so your tenant mix is not always the greatest. At the end of the day, I was like, “I need to scale up.” I started going after some larger apartment complexes. I bought a 48-unit, I bought 138-unit apartment. That was where I started to realize having a team on-site that can basically manage the asset versus trying to have a third-party management company manage it from afar. It just made a night and day difference from that standpoint.

Something really interesting happened to me. I was working on all these apartments and it was a lot of work. It was not easy. It was not passive by any means, so don’t let anybody tell you that that’s the case. I had an investor of mine who owned a ton of shopping centers and industrial buildings and couple of office buildings. One day I asked him, “Why don’t you own any apartments yourself?” He goes, “I don’t want to work that hard.” I go, “What do you mean?” He goes, “I only buy triple net lease deals.” I go, “What’s that?” He goes, “Where the tenants pay and your taxes, your insurance, and all the common area maintenance. Anything that’s interior in their suite is their problem, and everything that’s exterior gets billed back to them.’ I was like, “That sounds amazing.” When a tenant beats up my unit at my multi-family property and leave it trashed, the only thing I can really do is evict them and go after them in the courts, which is usually cost me more money and time than it’s worth.

I was like, “This sounds really intriguing.” That’s when I really started to dive into the commercial sector where I then went off and bought an industrial building, a medical building and a shopping center. I just loved it. I remember you sign a lease, you add a couple of hundred thousand here, $500,000 there, $1 million here, literally with a signature. I was like, “This is incredible. Now it’s financeable. I can go to the banks, I can refinance before the tenant’s even in and operational. I could go refinance and if I needed to do tenant improvement and I can borrow that.” It was just a whole different mentality. I call it the evolution of real estate investing where you might start off with like single-families, then you scale up to apartments.

It’s a really easy concept to go from single-family to multifamily. Going over to the true triple net stuff, it was a learning curve. It doesn’t happen overnight. It’s a different language. You just underwrite deals much differently. Everything from leasing to the way you stabilize these things is just different. At the end of the day, I just fell in love with it. I really feel like I found my niche within retail and industrial and that was the beginning of a long-term business plan and what we’ve been focused on over the last decade.

Yeah, that’s good stuff right there. The evolution of real estate investing. I just exited like 35 units between two buildings. The 1031 exchanges are still open. If they don’t close, I don’t care, I’ll pay the tax. I’m in this I odd place with that. There was this false sense of security, Danny, in owning those buildings, like, “I’m paying them down and someday they’re going to be better rents,” and the whole thing. If you do the math on the turnovers, like the fifteen-unit building, while I was under contract to sell the property, I think like five evictions started, so it’s like a third of the building. They might have worked it out and got them paying again. I did not even look. I was so at the end of my rope with that.

As I look back through the ownership of both those buildings, every year, every penny of the cashflow was vaporized by 3, 4 or 5 months of no rent. While I’m getting a tenant out of there, I’m paying to do the turnover. I’m paying a leasing commission again to get it full. Maybe I’m evicting the same tenant in like month nine or something of the new tenant.

I don’t really know if that was the case or they were the old tenants. I didn’t even bother to look that close. I say it’s a false sense of security. This is probably C or D-grade, like you said, the rough apartment areas to own. Maybe it was an asset class thing. Multifamily investors laughing at me right now. “What an idiot Dan Breslin is for investing in the wrong class.”

I think there’s a sense of freedom that comes from that. My money’s now, I don’t know, 70% as far as like my net worth. Industrial, self-storage. We’re doing self-storage development as we speak. The center that we own together, those are passive for me. The partners are doing all the leasing. The partners are overseeing the construction. There’s a quarterly management statement that comes out or partner report, I guess it would be.

It’s just weird to have that false sense of security that’s like fictitious. There is net worth there. There are large checks that came from the sale of those apartment buildings. There’s profit there, but the actual ownership of them was such a break even, if not negative, tens of thousands, maybe $100,000 depending on how much repair had to go in a given year. It’s just got to be really hard to sustain that versus the triple net lease into the industrial. That’s like some of the pain. I’m done with the pain of those apartment deals.

I’ve got to tell you, I got into real estate because obviously the book Rich Dad Poor Dad was like, “Assets put money in your pocket every month.” I never realized that with apartments. I had a couple of apartments that did okay, but for the most part, the portfolio was break even if not negative, constantly. It was a never-ending battle. It wasn’t until I got into triple net, the triple net business that I really started to see what coupon clipper cashflow, Steady Eddie.

You can project it out for many years in advance of what you’re going to get based on your rent roll because the tenants don’t sign twelve-month leases. They sign 3, 5, 7, 10, 20-year leases. People always talk about this. I always hear it out there, “That’s really risky. What if they go out of business and this or that.”

It’s like, “Yeah, that happens,” especially for people that are just starting. We gamble all the time with that knowing that we can turn that space around very quickly, and eventually we’re going to get somebody in there. When you find the right operator, they typically are in business for a long time. We’ll find a nail salon, for instance. They’ve been around for a decade and it’s like they’re humming along, they’re doing great, they’re financially successful they’ve got good clientele.

They’re not going anywhere. I don’t see that industry changing. We’re primarily focused on the industrial and small bay retail. We just know that we can backfill that stuff so quick and easily compared to trying to backfill a grocery store box or a 100,000 square foot logistical building like that. There is a lot more time and money involved to get those spaces leased versus 1,000, 2,000, 3,000 square foot box. With the apartments, I just never realized the cashflow. I always wanted passive income. A goal of mine was like, “I want to get to X amount of cashflow so I can live a certain lifestyle.” The apartments just didn’t do it for me. I always made my money when I sold every time on apartments.

Ditching Long-Term Leases

Here’s another part of the growing pain I could share of my own. When I first started buying houses and renting them out and apartments and renting them out, one of the fears I had was what if somebody doesn’t rent this house, which just sits vacant? I’ve driven by vacant houses, like for a decade, 15, 20 years. Houses sitting vacant. I assumed that was a risk I would have in residential real estate. That did not at all turn out to be the case for any of my units. 30, 35, 40, 45 days on the market for a rental was a long time, no matter if it was a single-family house or an apartment unit. Granted, we’re in bubble epic bubble times of real estate in all of history for the United States.

When you find the right operator, they will be in your real estate business for a long time.

It may not have actually been you turn around your unit and get it rented in 30 to 60 days. That may not have been reality a decade ago, 15, 20 years ago, I don’t know. It doesn’t really matter. I got comfortable with that speed and that timeline. We just did a triple net lease on a single tenant warehouse deal. On March, we just got our first rent payment. We were vacant for like four months. I think we may have been 6 to 7 months on the market.

We went on the market for 6 to 7 months, and we filled 30,000 square foot space with a decent enough lease. That felt slow to me, Danny. I am so used to speed in the residential game. It’s like houses are liquid. Apartment units are liquid. It’s the small bay industrial and small bay retail sector. What is the average days on market timeline when you’re going to turn that unit and backfill it quickly?

I’ll tell you, it’s a lot quicker with small bay industrial. If you’ve got 1,000 to 3,000 square foot bays with a small 500 square foot office, one bathroom and just warehouse space, we typically will have a waiting list, if we get it out there on the market, never more than 30 days for the most part. Those stuff leases up fast. We’ve had great success in that. We’ve had great success in getting the lease rates up.

Typically, like even on those on the true small bays stuff, we don’t even like to sign long-term leases anymore because the lease rates have been going up faster than the 3% that you would typically put on a normal lease. If you’re signing a 3year lease at $10 a foot, and then you add 3%, that’s only $0.30 a square foot a year.

We’ve had it where we’ve gotten $1 or $2 every year in increases on a property. Yeah, on some of those, we like to do shorter term just so we can get it to market faster. Anyways, on the small bay retail stuff, it depends. I will tell you, if you’re holding out for nationals, that can take a long time. The holding out for a national, if it’s even national-worthy, every center’s different depending on your ingress, egress, your density, your rooftop density, your traffic counts, all these different things come into play. From start to finish with the national tenant, it can take three months. I’ve had it take almost a year from start to finish. When I did a Starbucks deal, that was about a year.

To clarify, Danny, that year was the moment the agent first looked at the site?

Yeah. They identified the site and said, “We’re interested.” It took a long time from start to finish.

To sign the lease?

It was just a piece of dirt. We had to do a whole build to suit. We actually had to negotiate what is it going to cost the landlord to actually build the structure for Starbucks and deliver keys to them where it’s basically move in ready? There was a lot that went into that into that process. If it was already a box that was ready to go and all they had to do was move in, it would’ve been a lot quicker. This was a true built to suit.

If you’re going with mom and pops, it can be quick. Even like on our deal that we’ve got together, we had a lot of mom and pops move in and we’ve had a couple of them not be successful and not make it, but because the units were rent-ready, they were turnkey, essentially, when we got it they were second gen spaces, they needed some work, so we had to go in there and clean them up and build them out.

Now that they’re built out, if that tenant doesn’t make it, there’s typically a lot of people that can come right in and literally just take it as is or very little build out at that point. That could be anywhere from 30 days to maybe 90 days. For the most part, when you’re dealing with these mom and pops, you can sign a lease pretty quick. A lot of times, they’re like regional tenants. Maybe they have 1, 2 or 3 locations around town. Those are just a lot easier to get done than a national tenant.

On the build out, that could be recycled. Are we talking like there’s a half bathroom, maybe two bathrooms in there, and like a counter from the tenant who failed? What type of actual build out is there? You’re not just like re-white boxing it all over again. Right,

Right. I’ll give you an example. We have this liquid. It’s called liquid. They’re not making it. We’ve got actually like two other tenants that there’s just not enough hood space in the market that’s open and available for these little restaurant tiers to come in. If you’ve got a hood and you’ve got basically a move in kitchen ready to go there is a hand, there’s a waiting list for those type of suites.

You put it out there and you’re going to immediately start getting action, and then you get to sift through and decide, “Who do I want to put in the center? What’s going to be the best fit? Who’s got the best financials? Who’s got a good forecast or has existing experience and other locations? You look at all those different factors and to determine who’s going to be the best fit. Yeah, like something like that. We don’t even have it out to market, but we already have a list of tenants that would take it like that if it were available.

I assume that TI was your responsibility originally to put the hood and the kitchen in? What’s that number?

It depends on the build out. Call it $20,000 to $50,000, probably in that range.

Lease rates are going up faster than the 3% that you would typically put on a normal lease.

Is it normal for the landlord to do that for those type of tenants?

Two Types Of Landlords

Yes and no. I’ll tell you the difference between us and other landlords. There are two types of landlords. One landlord, which we love buying from, is the type of landlord that doesn’t give their tenants any tenant improvement dollars, doesn’t fix up the property and essentially wants to lease everything as is to anybody coming in. Whoever’s coming in is going to put the full investment into the space.

Here’s where I see the value and why we don’t do this. They’re typically going to get, we’ll just call it market rate rent for an as is space would be $10 a foot. If we go in there and we do the tenant improvements and do the build out, we may get $20 a foot for that same space. When you look at it on a cap rate, we might be creating $6 to $10 for every dollar we put in the building or in the build out.

If we’re going to go put in $100,000 in tenant improvements, I’m hoping that that increased the value of that space by $500,000 or whatever it might be. It’s going to be significant compared to the investment in the space. If we’re handing it over turnkey like that, we’re going to demand a much higher rent, ultimately resulting in a higher value of our property.

You got the benefit of the backup plan. If they fail, that equipment is yours and that tenant is not scrapping all the equipment they put in there and turning over a box again that needs a bunch of work. How often have you exited? When I’m underwriting shopping centers myself, I can see the TI packed rents in there. No, we’re not getting $34 a square foot for this space. It’s just not happening. The market does not demand $34 a square foot. It might demand $15 or 417, but there’s a TI package in there. Sure enough, there is some kind of TI package in there. That makes me hesitant as a buyer to want to pay NOI type of income on some of that TI dollar for dollar. Have you been successful in selling that to the next buyer and getting full freight on the cap rate and the TI rent?

Yeah, so I’ll tell you, we don’t like to do that in general, where we’re way beyond what the market is because anybody’s going to come in and underwrite and say, “All the other shopping centers in the area, lease rates are between $10 and $20 a foot. If you’re at $34, you’re just so far off the mark. Anyone who’s going to come in is going to discount that.

We be at the higher end of market, whatever that is. We don’t want to be above that because then yeah, again, we’ll get dinged on it on our exit. We are conscious of that. There are certain occasions that you’re going to get a higher rent and you’re just like, “If I hold it, I have a higher cap rate, better cashflow,” and if I want to flip it, you just got to come to reality of what the market is and what someone’s truly going to offer you and you’re good with it then great.

How much of a discount will the bank ding you on the refinance for that $20, $24 a foot for the built out TI space? Are they also taking some off of that income?

Typically, they’ll be a little more conservative on it. It’s typically like a give and take. You can go back to the appraiser, you can go back to the bank and say, “We did all these finishes.” It is like a nice restaurant. You go into some restaurants and they have a couple of hundred dollars a square foot and tenant improvement you can see. You’re like, “This is really nice.” You go into the other guy and they’re $20 a square foot build out, and you can tell.

There is an argument to be had and to be made for that. That’s just really laying it out for the appraiser and for the bank and letting them know. It may not even be like your comps are on this street, but if you’re in a city and you can point to other restaurants that are within the city and say, “Here’s a comparable build out and their valuation and what it traded for.” Instead of looking at it from more of a localized aspect, you’re looking at it from more of a macro point of view.

Working On Short-Term Leases

You build a nicer house with nicer finishes, it should appraise for more. You spend $650 a foot building a house versus $185, clearly that’s a multimillion-dollar home versus the starter home. That’s logical. Danny, where do you fall on the buy and hold forever spectrum versus everything is sold as soon as it’s baked and ready?

Some investors that we would hear about are like, “The guy held everything forever. He is 90 years old, he’s got $100 million in real estate, and it’s all paid off. On the other end is nothing’s probably in portfolio more than 49 months and it’s all sold. A lot of times, to pay investors off and keep it going. Where on that spectrum do you lie in general? I know that deal by deal is clearly going to be impacting that.

I have two buckets. The fix it up, fill it up and flip it, and then the long-term hold, refinance, and hold it. It’s been different lately and the market’s constantly shifting. I will tell you, from my standpoint, if I don’t have any partners or I only have like 1 or 2 partners, I love the idea of holding long-term, and especially if I love the asset, love the area. In the beginning of my career, I’m guilty of selling way too soon because I wanted to, number one, pay off my investors, number two, get some cash in the bank as I was building up my nest egg. Now, we’re looking at stuff on a long-term hold aspect.

When we come to the point where it’s ready to either exit or refinance, we’re looking at the market conditions. Right now, it’s not the best time for long-term fixed financing putting 10-year debt and you’re going to be at 7% plus. It’s not as attractive, obviously, as it was years ago. It changes the projections of what you were looking to do. For me I am still holding quite a few things for the long-term. They’re not in big syndications or they’re smaller deals. Not all smaller deals, but smaller partnerships. For larger syndication, unless we can refinance and pull out a majority of the cash, we’re probably flipping out of it, for the most part.

Some of these I’d love to hold long-term and it might be one of those things where we’d go back and say, “We’re going to go in for a refi. Who wants to stay in and who wants to get out?” That could be a conversation had. I definitely agree with you that there is something to be said for never selling. I have partners like that and they’re some of the wealthiest people I know. Cashflow is amazing. They can live any lifestyle they want. I’m trying to do more of that and just really build up a really quality portfolio that never sell. We do a lot of deals though, so we’re constantly recycling money and then we’re holding certain things. That’s why I say I have two buckets. It’s nice because one generates cash and the other one generates cashflow.

When I get residential houses, you’re fixing and flipping, there’s a finish line and it’s 6 to 12 months from the day you go to settlement on the A to B purchase. Fast, transactional, in and out. If you’re going to build a portfolio of houses, 10, 12, 50, 100 or more, if you’re going to buy apartment buildings, if you’re going to buy any of these assets that we’re really talking about here with maybe the exception of to build a suit Starbucks, which is a little bit of a set it and forget it. Less of a business, more of a real estate investment. These are businesses, Danny. Every single one shopping center that is valued at $15 to $20 million is a business that has to be run. It has to be managed. Someone has to do the snow, somebody has to do the landscaping, someone has to renegotiate the landscaping contract.

Always know the real estate deal you are getting into. If you are not careful, you can get into something that looks amazing but could become your worst nightmare.

Someone has to drive by and make sure the landscaping contractor actually did the work. It’s a never-ending business. It’s almost like you could apply the Warren Buffet mindset to any of these assets as well. It’s like, which of these businesses has a moat in the form of the location, has a competitive advantage due to the traffic patterns that exist for that specific business. It’s an advantageous piece of real estate and maybe it’s an advantageous tenant mix that you put together. This thing is just working magically.

You would really regret selling that one later if it turned out to be this quality business in the way that Warren Buffett might talk about it. Whereas on the other end of that is there’s probably a whole lot of other subpar businesses that somebody wouldn’t want to own where they have to go out there and run the lawnmowers themselves in the landscaping thing all the time versus somebody who’s built up some team with 100 trucks and 100 teams who are doing the lawnmower.

The larger scaled up business would be one you’d want to hold forever and a smaller mom and pop one would be one that maybe it is worth buying that one for $1 million, putting in some marketing, putting together the business and, and fixing it a bit, and then selling it for $3 million and making the check and keeping it moving.

I think when I realized that my rental portfolio was a business, and the reason that I sold most of it already is I knew that I didn’t have the time and bandwidth to apply building a great business to manage my own real estate while I was in the middle of building, running and managing Diamond Equity and flipping a couple of hundred houses a year. I made a decision that my energy was going to be a better return on time for me and my partners in the main business. That was what is driving me to sell the rest of that portfolio off.

It’s like this concept for me of looking at every one of these balance sheets, the rent roll, the income, the expense. It’s a complex business, maybe not as complex as some other businesses that you might buy. We can analyze the risk in these commercial real estate assets, these commercial real estate businesses one by one, and you can see the comps a lot easier, and you can see the potential for the income a lot easier to mitigate the risk compared to other businesses. At the end of the day, you’re buying an operating business and maybe the seller didn’t realize that’s what they had, and you’re implementing these systems to build the value there. Holding onto the great businesses for the long haul, the great assets is a great place to be.

I have a friend who who’s owned a lot of property. Maybe half a decade ago or something, I asked him, I go, “How do you know when to sell versus hold?” He goes, “Danny, you never really know going into a deal. I can’t tell you why or what, but you can get into something that looks amazing and it becomes your worst nightmare. One problem turns into another, which turns into another, you solve one another one comes up. I can’t tell you why, but those ones, after about a year or two, you’ll figure it out if it’s a holder or if it’s flip out of it. It’s his philosophy.

It’s just really you might buy something and it’s just Steady Eddie. You spend very little time managing it. There’s no headache involved. It cashflows really well. He goes, “Those deals you just got to hold on for the long-term. You’ll know a year or two in.” That’s an interesting thought. You think you’re going to go into something and hold it forever, but I’ve had those properties and they just one headache after another. That’s been something I’ve implemented somewhat into the buy and hold versus buy and flip model.

Least Amount Of Money Put In A Deal

I love that rule. What’s the least amount of money you’ve ever put down on a deal excluding, “We raised $5 million for this, or whatever, so I didn’t put anything in there.” From a creativity standpoint, Danny, what’s the least amount of money you’ve had to put into a deal commercial?

I’ve gotten to a deal with nothing. Are you saying like I was able to borrow all the money with existing relationships that I have, and no partners? I’ve done deals like that. I’ve done seller financing deals. I’ve done deals where I literally got preferred equity and I got cash back at closing. I actually got a big check. I just closed a $15 million deal and my down payment was $866,000. Our year one cashflow is $260,000 with 2.5% rent bumps every year. I’ll have all my cash out in year three. I have an eighteen-year sale lease back on that deal. That’s going to be a nice long-term Steady Eddie. It’s going to be a good one.

Is there a personal guarantee on that loan?

No. Non-recourse.

You have the 866 at risk until that money’s back out of the deal and then after that, it’s smooth sailing.

I have risk for three years, but we got a CMBS loan on that one and then we had preferred equity from the sellers. There was a ton of background checks with this tenant. They’ve been around since the ‘80s. They were about $160 million in revenue in 2024. CMBS literally went through all of their ledgers, all their clients, called them all up, verified everything, and at the end of it, they said, “They’re as solid as a Starbucks.” I was like, “That’s great.”

Is this the Reading deal?

It is.

Sometimes, the only way a real estate deal would make sense is to reengineer it and make the numbers work.

Congratulations.

Thanks. Not that Reading’s great, but the tenant and the cashflow are fantastic.

There’s something to be said there because I am from Delaware County and Reading is like Berks County, so it’s probably about a 45-minute drive from where I went to high school to Reading, PA. Any of our readers in the Philadelphia regional, like, “There’s nothing at all worth $15 million at all in the whole city of Reading.”

I apologize to my Reading audience, if anyone’s there. The market’s actually gotten pretty freaking hot. I’m shocked at what properties are selling for in Reading. It is one of those beneficiaries of the market. What seems to be now that the housing shortage has pushed the demand into markets that didn’t have a lot, Reading happens to be benefiting from that. I think long-term you could see some change over there that’s helpful.

What I learned is it is so easy to judge a book by its cover in the commercial real estate business. A lot of money is made in areas, Danny, where the locals are like, “You never buy anything there at all.” I’m sure there’s a lot of people who take the call on that a deal and they’re like, “No, we’re not going to touch anything like that. Never going to happen in Redding.” On this specific deal. They would’ve never dig in a little deeper.

I was just throwing this out there. Think about all these qsrs that we see. These old Starbucks buildings, these old Carl’s Jrs.. Those buildings are crap. Especially if they’re over 20, 30, 40 years old and they’re still sitting out there, but if they have the right signature behind it, it’s worth millions of dollars. If it were vacant, it’d be worth a couple hundred thousand dollars. It’s all about who’s back in that lease and how long it is.

Maybe that’s the answer to the question that I was thinking. It’s like what made you want to dig a little deeper on that one as it as it crossed your plate in the first place?

Where that came about was when the interest rate market changed and shifted from the low-3s, mid-3s, and it went skyrocketed up to the 7s, basically, everything went stagnant in the commercial world and probably the residential world too for a while there. There wasn’t a lot of transactional volume going on. I was wondering to myself like, “If I can’t go borrow money at 3% anymore and I have to borrow it at 7% and I have to go buy that same deal at a 7% cap, there’s no spread, you’re not getting a spread between your debt and your cap going in, how do you make deals pencil or work?” We went a whole year without buying a single asset, which was the longest time I’ve gone since I started in 2009 of not buying a deal.

It was a dry spell. That’s when I came up with the concept. I said, “What if I could pay their price, get their cap, I’m the only buyer at the table, but I’m going to have them stay in for my equity? The way that I’m going to structure it is in a way that secures my position in the asset so that way, I’m not at risk if it doesn’t work out.” Basically, on that deal, it was a sale lease back and we use their equity to be our equity, giving them a return on that equity that was lower than the 7% caps. It was like 4% and it’s basically tied up for 18 years. If they ever stop paying rent, it gets wiped out within one year, it’s 5x damages.

Now my basis in the asset is no longer $15 million. It is $5 or $6 million. It changes drastically if they ever bailed or whatever. On top of that, I got non-recourse step for the first position loan. That was the only way that that deal would make sense for anybody. It was re-engineering it to make the numbers work. I said, “If we could do that on other deals, there’s lots of deals out there that are stagnant, sitting out there not moving, not trading, because there’s just no gap. The only person that can make it make sense is an all cash buyer.”

Who wants to do that on the stabilized sale leaseback deal at like above market cap rate basically, right?

Yeah, exactly.

Focusing On Small Bay Industrial Multi-Tenant Asset

What are your favorite asset types these days? 2025, in market now, what kind of calls are you looking to get right now as we speak?

Right now, I’m highly focused on small bay industrial multi-tenant assets. Call it somewhere between 10,000 to 100,000 square foot multi-tenant industrial facility where the unit sizes are somewhere ranging between like 1,500 square feet up to like 5,000 square feet. There can be some bigger ones, whatnot.

A lot of times, you can cut those back down though into smaller units, but I love the 1,000 to 5,000 square foot bays. That’s ideal, and then small bay neighborhood shopping center. 1,000 to 5,000 square foot suites in a neighborhood shopping center where you’ve got your Subways and you’ve got your taco shop and your barber. Those are what we’re looking for. Typically, everything we’re buying, there’s got to be some meat on the bone.

There’s got to be some value add, whether it’s vacancy, whether it’s below market rate rents that we know we can turn. A lot of times, the properties need work. They need to be really refreshing and cleaned up and properly managed. Yeah, we’re doing a lot of that stuff in the Rocky Mountain and Southwest. I call it the southwest Rocky Mountain region. Arizona, Vegas, Utah, Colorado, New Mexico, Texas, those are our primary areas of focus, although we do stuff around the country. We got stuff here and there.

How do you manage something, let’s say in Memphis, Tennessee, living in Scottsdale or Utah or somewhere that’s like a 6 or 7-hour plane ride?

Hold quality real estate assets for the long term especially if you got in on a really great basis. Just let time do its thing.

I couldn’t do it if it was a small apartment building, that’s for sure. With retail or industrial, typically, we’ll get some boots on the ground. A lot of times, it’ll be one of our tenants that gets a discounted rent or if there’s somebody local that we trust and we know. Maybe it’s even a management company that we’re not paying them the management fees because we run all the accounting through our teams and we run all the calls and field everything through our office so we know what’s going on. We have a handle on every property.

We like to have someone that is boots on the ground walking the property, whether it’s weekly or a couple of times a week. They’re reporting to us of what’s going on. If you talk to your tenants, they’re going to tell you what’s going on. If there’s anything weird going on or deferred maintenance, you’re going to hear about it. Yeah, having boots on the ground, I’d say, is the number one thing. You always want to find someone who can really be your eyes and ears on the ground and then you can manage from anywhere, really, as long as you know what’s going on. There’s no reason you have to actually physically be there as long as you have somebody that is.

Do you guys implement any technology like camera systems out in the parking lot or anything like that as a standard procedure?

Yeah. Camera systems are great, especially if you’re going to hold long-term. It’s worth the investment. A lot of times, we’ll either try and get one of our tenants to be our eyes and ears, and usually, when you do your tenant interviews, someone loves to be that person. You can tell pretty quickly they’re going to tell you everything about the center, everything about the property for the last twenty years, and you’re going to learn more than you ever would’ve looking at anything on paper. You ask that person, “How would you like to be our eyes and ears.” They feel like they’re really part of the community, part of the center. It’s great doing that.

Danny’s Book Recommendations

I’ve got a couple wrap up questions here that we ask all the guests. We mentioned Rich Dad Poor Dad. Excluding that book, are there any recommendations, or maybe it’s even a podcast or some other source of information that you think readers might gain a lot of value from, Danny?

For real estate, there’s a lot of good ones out there, but Real Estate Titans was a great book. It just talks about the titans out there that owned massive portfolios. Some of these REIT managers, fund managers, guys like Sam Zell. It’s super interesting to listen to it from a guy or from a lot of different titans out there that had multi-billion-dollar portfolios.

Danny’s Crown Jewel Of Wisdom

The crown jewel of wisdom. Danny, if you could go back to 2009, knowing everything you know now, what would be the crown jewel of wisdom you would share with yourself then?

Two things. When there’s a crash, when prices are dirt cheap, understanding lots of different types of real estate and markets as well is really beneficial because then you can just swoop up everything and swoop up as much as you can and hold for the long-term. I look back at some of these deals and I’m just cringing at why I sold too soon. Not just even holding for cashflow because the cashflow a decade later, just looking at it, would be absolutely game changing. I’m like, “Why did I sell?”

At the time, I’m making a couple of hundred thousand or $1 million or whatever, and like, yeah, it felt great in the moment but to look and see how those assets are now performing, you cringe a little bit thinking about it. I would say going back to the philosophy of holding the really quality assets for the long-term, especially if you got in at a really great basis, just let time do its thing. With inflation in your rents, it is just going to be incredible cashflow. If I would go back, I would’ve gotten a true triple net leases sooner and I would’ve built a little bit of a team sooner and I would’ve held a lot more.

Where can readers get more Danny Newberry?

They can reach out to me. Our website’s VailCommercialGroup.com. We do a lot of joint ventures. We do a lot of partnerships where somebody who may need help with financing or signing on debt or bringing capital to a deal management, whatever it might be in a project. We’re always interested in getting involved in stuff that meets our criteria, especially if it’s in the Southwest or Rocky Mountain region. We do a lot of those type of partnerships and you can reach out to me at [email protected] and we can schedule time to talk.

The final question I ask all of my guests, what is the kindest thing anyone has ever done for you, Danny?

That’s a tough one. I really got to think about that. I’ve had a lot of things in my life. I’m very blessed to say that I have great people in my life. The kindest thing is my mother bringing me into this world. Can’t beat that one. Mom, thank you.

It’s a great place to start and a great place for us to finish. Danny, thank you for coming on the show. I got a couple of pages of notes here. I had a had a good time. I really appreciate you joining us here.

Yeah. It’s been awesome. Thanks again for having me on. I really appreciate it.

Danny Newberry is the founder of Vail Commercial, focusing on commercial real estate investment and management, particularly in small bay industrial and retail spaces. He is known for his strategic approach to identifying value-add opportunities and is a respected thought leader in the real estate community.

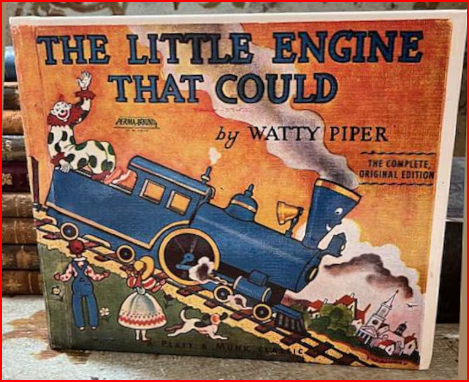

One of my first memories in life was my greatest loss. This happened somewhere around 2 or 3 years old. My favorite book at that age was The Little Engine that Could. I must have brought that book everywhere with me-so it came to pre-school on that fateful day.

Mom picked me up but placed the book on roof of the car-then drove off. The book disappeared and I was distraught. We looked around everywhere back then, but couldn’t find a replacement copy. I don’t remember the details of the event or the time period, but I still feel the sense of great loss. That feeling of loss exceeds any of the monetary losses I’ve experienced (some of which exceed 6 figures).

Alas! A Lifelong Win!

“I think I can-I think I can-I think I can-I think I can-I think I can-I think I can-I think I can-I think I can-I think I can.” This is all I remembered from The Little Engine that Could. What a fantastically strong belief system to install in the mind of a 3 year old! Most of my life, this mantra has applied: “I think I can!”

Faced with any challenge, “I think I can!” Considering executing that first fix & flip, “I think I can!” Build a $15M development, “I think I can!” Hoping to win that next deal, “I think I can!” Once any challenge has been met, this becomes, “I know I can, because I’ve done it before.”

(Aside, as I researched an wrote this, I am now realizing my mom might has simply gotten rid of the book to avoid my likely endless requests for her to read it to me… As an adult, I’d completely understand this now if that was the case. You can see why if you read it yourself.)

I Think I Can – MAKE A DEAL!!

Here’s an example of how this created the life I live now. I am a Deal Maker. Any deal begins with: “I think I can win this deal,” and therefore I make an offer. If you don’t believe you have a shot at winning the deal, you’ll never make the offer.

Further down the track on Deal Making is your follow up. Again, “I think I can win this deal,” and therefore, I follow up. If you don’t believe you have a shot at winning the deal, you’ll never follow up. In Diamond Equity’s experience, about 45% of deals occur 30 – 1,819 days after the offer is made. That is a long, strategic follow up cycle requiring a strong belief system to stay the course.

Next time you consider a deal, remember, “I think I CAN win this deal” and MAKE THE OFFER! And when the offer isn’t immediately accepted (which is 99% of the deals that get done..), remember to follow up diligently and earn that deal!

Seasoned real estate investor and entrepreneur Fernando Angelucci is here to break down his strategies for finding success in self storage development. Joining Daniel Breslin, he presents their three-point approach, like three legs in a stool. Fernando explains how he considers location, technology, and the current market dynamics in choosing a self storage to invest in. He also shares his experience in dealing with zoning risks and how to handle new real estate development versus retrofitted properties.

This Episode is Also Sponsored by the Lending Home. Lending Home Offers Reliable & Low Cost Fix & Flip Loans with Interest Rates as Low as 9.25%. Buy & Hold Loans Offered Even Lower. Get a FREE IPad when you Close Your First Deal by Registering Now athttp://REILineOfCredit.com

Fernando Angelucci & I Discuss Self Storage Development:

Current Market Trends (00:03:21 – 00:04:22)

Innovative Business Model (00:11:55 – 00:12:37)

Investment in Technology (00:19:50 – 00:20:30)

Long-Term Vision for Investment (00:36:20 – 00:37:30)

Engaging with Municipalities (00:46:30 – 00:47:48)

I’m doing well. I’m in Florida. For whatever reason, I love location stamping my episodes. I ask most guests where in the world are you recording from?

Yeah, I’m currently recording from Curitiba, Paraná in the South of Brazil.

Navigating The Self Storage Space

One of the more interesting locations we’ve heard for sure on the show. For readers who don’t know probably some of your story, if you could start there, would be how Brazil and South America ties in with Chicagoland, which is how I know you is, because you’re aware of this local guy who’s not quite as local as may have originally thought.

I’m the son of two immigrants from Brazil. This city is actually where my dad was born. I have family here. I’m taking care of one of my family members right now. The story moving forward is my dad went to the United States. He was an engineer. My mother also went to United States at a different time. They actually met in church in Chicago and then I was born and raised there.

I went to school there. I ended up going to University of Illinois, graduating, also becoming an engineer. Prior to that I read Rich Dad Poor Dad when I was sixteen years old. It changed the whole way I thought about making money, especially the way that my parents taught me how to make money. Their old school American Dream was go to school, get good grades, go get a job at a Fortune 500 company and then retire the pension within 40 years.

Obviously, that book tells you to do the exact opposite of that. I lasted about thirteen months in the engineering world. I immediately started flipping houses, wholesaling contracts, buying rental properties, buying apartment buildings. Around 2016, I started to see this trend where the government started getting involved in habitation-based real estate in private investors businesses. A perfect example of that’s during COVID when they basically told tenants that they didn’t have to pay their rent and you couldn’t do anything about it. You couldn’t evict them. The investors, they still had to pay their mortgages and property taxes or else they would lose their properties.

Just to interrupt you a second there, that trend is probably more prevalent as rent control across the country. It’s been popping up for a long time. It is law in a lot of markets. It is hanging looming threat in a lot of markets. In some markets, maybe it’s not at all on the radar, but with the housing shortage and with the prices of homes and inflation, I think that threat has certainly crossed every residential real estate investor who holds rental property that way. It’s probably crossed their mind and maybe one of them things that could come up at any minute anywhere in the country.

We always thought it was primarily just going to be in LA and New York City, but then you start seeing it creep into the like the Midwest where your really good rental properties are. The really good returns. Look at Minneapolis now. I think that it’s one of the most hardcore tenant friendly cities in the country now, even above New York and Los Angeles because of the rent control, the restrictions on being able to raise rents until you do some substantial amount of rehab.

I know a lot of investors that they ended up having to sell all their rental properties in that market because it just didn’t make any more sense to hold them there. That was a tough trend to see. When we started seeing this trend closing in on Chicago and the Midwest, we decided, “What’s a good asset to get?” We started looking at things that are instill in real estate but does not allow someone to live inside of your investment. It allows much more control and a much lower amount of risk or risk mitigation for ourselves and our investors.

We came upon three things. It was data centers, mobile home parks, and self-storage. Right off the bat, data centers were out because to build a reasonable sized data center, you need something like $150 million in equity and then small data centers like a $500 million data center. That was out. I knew a lot of investors that were already in the mobile home park space. I called them and said, “What do you think about this?”

They said, “Fernando, listen. On paper, yes, they claim that mobile home parks, you just own the land. You don’t own the property, you’re never going to be a landlord, but in reality, you end up having a lot of park-owned homes and you become a landlord again and you’re renting those park owned homes to the tenants.”

We scratched that and then we were left with self-storage. As I started to dig in, I started to see that the numbers for self-storage were just absolutely fantastic. Not only from the way that the state law treats our asset class, so codified in state law, but then also the way that it reacts in recessionary environments. This is a very apt time to be doing this episode because I think the S&P 500 has dropped at about 10%. It is very recession resilient asset but it also does very well when the economy is doing well because people start buying more things, they start storing those things.

When the economy is not doing so well, it’s called the trauma and transition business, when you’re downsizing houses, when you’re moving in with friends because you can’t afford your rent anymore, when you’re changing locations for a job, when you get divorces type of stuff, self-storage does really well.

Self storage does really well when you are downsizing houses, moving in with friends if you can’t afford rent anymore, changing jobs, or getting a divorce.

For example, during COVID, which is probably the biggest recession we’ve seen in recent times, self-storage was operating at a 80% year over year rent growth because the amount of people that had to move stuff out of their houses to create a home office or to create an area for their kids to go to school virtually and they put all that stuff into storage. It worked really well for us.

Same thing when you look at the last major recession, the great financial crisis of ’07 to ’09, I know you were very active during that time, the S&P 500 dropped 22% over that period. During that time, self-storage only dropped about 3.4%. That’s a minor hiccup to swallow compared to say your portfolio just being wiped out.

The self-storage, I think the demographic I heard was 80 million Millennials now became the largest demographic that we have active. That’s you, that’s me. That’s all the age group probably between your age, my age, who’s reading. It’s like 28 to 34 or something like that. Anyway, they’ve hit their peak earning years. This is why we have a housing shortage because there is the largest number of home buyers reaching that age, getting raises, moving up the ranks at their employers at finally at 35 and 40 years old. These people have tons of stuff. I look around my own house. I’m trying my best to be minimalistic and frugal but that Amazon truck just comes 3, 4, 5, 6 times a day sometimes. I think you’re also going to see a lot of this self-storage demand continue to come from people just buying more shit.

We have such an easy method in society in 2024 compared to 2004 to have stuff delivered. The Millennial expectation is I push a button on my phone and it’s there in two days. That is for me. I’m like, “Amazon can’t deliver this for two days? What the hell’s the hold up here?” That’s not how it was back in 2004 or 1984 or 1994. I think the ease and ability to get crap delivered to your door is a tailwind yet to be born out in the demand of self-storage. I think we’re going to continue to see that growth of storing stuff for people’s inability to part with the stuff that they’ve then collected.

I think that adds to another crisis that again started during that great financial crisis where a lot of contractors went out of business and decided never to come back. A lot of appraisers went out of business and decided never to come back. The amount of new homes that they were delivering dropped off a cliff. We have yet to catch up.

If we build in it on top of what we’re already building, if we build an additional million homes per year, it’s going to take another ten years before we’ll finally get to a point where supply will meet demand. In addition to that, you have this inflation that we’ve experienced over the last twenty years that has caused home prices to go through the roof. I’d call it 7% interest if you want to buy a home on a 30-year loan, but compared to that same home 20 years ago, it is now 3 or 4 times the cost.

What are people doing? Instead of opting for the 5-bedroom ranch in the suburbs, they’re getting a 2-bedroom apartment in the middle of downtown because then they don’t need a car. They can take public transportation, they can walk these walkable fifteen-minute cities, if you will. What are they going to do? Instead of having those extra three bedrooms, they’re just going to going to store everything that they don’t use on a daily basis in a self-storage unit. The things that they use maybe on the weekends like mountain bike or a kayak or whatever, you’re just going to go into your storage unit on the way out and pick that up and then drop it off before you come home.

Let’s say in summertime, instead of keeping all your winter clothes in your house, you’re just going to leave them in the storage unit. As the seasons shift, then you’re going to switch everything out. Now storage facilities are being used as like a second or third or fourth bedroom that these Millennials can’t afford now like their parents could during 20 or 30 years ago.

To build the houses now with inflated material costs and make a 7% interest rate work with the builder, the developer doing some rate buydown, they have to cut costs somewhere. That means where they used to be able to put a basement in there, they can’t afford to put the basement. That means where they would get 2,400 square feet a few years back when things were cheaper to build and finance, now maybe you’re getting 1,800, 1,700. Maybe you’re getting 1,100, 1,200.

It’s funny, you can go back through time, if you pay attention to all the public records that you look at in single-family houses, you can see how the economy was doing at different points in time. If you look at like a 1933 built house compared to like a 1926 built house, the 1926 is likely going to be a little bigger. They use stone versus brick or stone versus frame and stucco. A lot of little nuance details.

Fernando’s Current Business Model

You could track that and look at that almost like rings in a tree to see the age. That’s how the rings of the real estate market exist in the public record. You can like see how much water do we have in the economy at that point in timely. Fernando, let’s switch gears a little bit here. Would you mind giving us an overview of your business model and what keeps you busy and excited now?

Yeah, so at SSSC, we are a self-storage developer, wholesaler buyer. We do value add. We have three main legs to our stool. In the last six and a half years, we’ve done 56 properties combining to value of around $255 million. That’s across 24 states. The first leg of the stool is the aggregation play. Right now, almost 70% of the self-storage facilities in the United States are owned by mom-and-pop operators. These are people that own two or fewer self-storage facilities, something that is considered non-institutional.

The top six publicly traded companies in the self-storage space, they only own 18% of the entire stocks and they obviously want to grow that share. What they’re trying to do right now is buy more and more facilities from these smaller operators, but they don’t want to spend the time the manpower, the Ivy League salary for their data analysts to just work on one facility.

They would rather buy a portfolio of facilities because it’s roughly the same amount of underwriting costs from a manpower standpoint looking at 1 facility versus 20. That’s our first leg of our stool. We’ll go into these mom-and-pop facilities, we’ll buy them, we’ll expand them so that they’re institutional in size, which for us is usually like 60,000 square feet or larger.

We’ll will increase the revenue by using artificial intelligence to see what our current customers can pay and what they can absorb if we were to increase rents and how much we should increase rents per person. We’ll also do competitor analysis to see what is the market in the area. What are the competitors charging, are they losing clients? Are we able to steal clients away from them? Then the second half of that stool is then dropping expenses.

When you work on things at scale, you have economies of scale so you’re able to get better pricing on insurance. You can afford better attorneys to fight your property taxes, your operating software, you get better deals on those. You’re able to drop expenses that way. Not only are we increasing the size of the facility, but then we’re also increasing the net operating income, which commercial real estate is valued. The commercial real estate, the value is based on how much income it could produce.

What we do is once those things are stabilized, we put them into portfolios of 10, 15, 20 properties at a at a time. We sell off that basically done for you portfolio to a publicly traded REIT or a private REIT because they have a much cheaper cost of capital than we do maybe they go raise a bond for less than 1% in Europe, maybe $500,000 or $500 million bond. They have a line of credit with Blackstone or Barclays that is substantially lower than what you or I can get when we walk into a bank. They’re able to pay much more and still double their money. For example, if your combined cost of capital is 2.5% and you buy something at a 5% cap rate, you just doubled your money on that investment.

They can’t have 2.5%, 1.5% cost of capital in this market, do they? It’s got to be a little higher right. Do you think bonds are selling for 3.5%, 4% right now?

Yeah, I’d say new bonds, but that doesn’t mean that they still have money that they need to outlay that they raised before. For example, Extra Space used to be I think the number three operator. They went to Europe and they offered a 0.875% bond to the European market and raised something like $500 million. What they proceeded to do was buy life storage to then leapfrog into the number one position as the largest operator in the country.

Do you know when that was that they issued that bond? Was that like a few years ago and they got it off 2022 or something like that?

I think it was when rates were still, fund rate was still like between 0% and 0.25%. That’s their equity. Their equity is less than 1% and then now you have the debt that was available to them during those times and I’m sure they locked in some pretty large amount of debt on revolving lines of credit. Their cost of capital is still substantially lower than say you or I

The whole point of that first leg of the stool is buy properties that they are not interested in buying on an individual level, increase the value add, increase the size, put them into portfolios, and now all of a sudden, when you put a $50 million price tag on that portfolio across 15 deals or 10 deals, then now they’re interested in in acquiring those.

It’s a classic private equity roll up strategy. That’s how private equity works. They have five businesses, each of them doing $1 million in profit, now you have a business that’s doing $5 million in profit, you could sell it up the chain to the next larger private equity firm who’s looking to buy $10 million, $5 million profit businesses all in the same space and then sell them up the chain again. I guess at some point, they end up on the stock market. Very interesting. The first leg of the stool is the aggregation play. What comes next?

The problem with the aggregation play is that these are facilities that are relatively small. We’re talking about when you first buy them anywhere between 30,000 to 35,000 square feet, up to 60,000 to 65,000. These large reits, they also want just big properties, especially in areas that are underserved. What we’ll do is we’ll buy land in hot markets like Lawrenceville, Georgia, Mokena, Illinois, and then we will develop a Class A state-of-the-art high tech facility that can be anywhere between 100,000 to 120,000 net rentable square feet.

One building that’s 2 to 4 stories tall is the equivalent of buying 5 individual mom and pop facilities or 4 individual mom and pop facilities. That’s our more aggressive play because no cashflow’s coming out of the deal for the first three years, but there’s a large pop on equity at the very end when we sell off the stabilized asset or the fully occupied assets to one of those publicly traded companies.

What is the third?

The third part of the tool is what ended up becoming an opportunity for us right after COVID. You were just talking about how easy it is now to go on Amazon, click 3 buttons and then in 2 days, something shows up to your house. During that time that was really hurting all of the retail stores. Sears buildings, Circuit City, Best Buy, things that usually people used to go out in the car to go looking, get a TV, etc. Now you can do that all online.

What we end up seeing is that these large buildings, 100,000 to 150,000 square feet that originally were leasing out at $6 to $9 a foot per year are now willing to sell that entire envelope for $9 to $15, maybe $20 a foot. Now we’re able to have an envelope that’s already up and that did two things. It solved two problems.

The first problem is during COVID, we had a supply chain issue where we could not get materials. If you needed conduit, if you needed RTU units, in some cases, if you needed concrete or asphalt, you just couldn’t get it. If you could get it, then you had massive pricing volatility where, at some points, right after COVID or during COVD, steel prices and wood prices jumped 300% to 500%.

That is really tough when you’re building a facility that is primarily made out of steel and brick and concrete. It’s difficult. If you can already buy a building that the envelope is up, then all you really need to worry about is putting the units on the inside and making sure that it looks nice and clean and well lit. That allowed us to do one thing, which is it dropped our time to completion by anywhere between 30% to 35% and then it also dropped our total cost to build by anywhere between 25% to 35%.

That was the third leg of stool. Nowadays, not much opportunity in that space. Out of all of our deals that we’re doing at any given time, that’s probably 10% or less now. Whereas after COVID, it was like 40% of our business. There are still some opportunities out there where people were just trying to hold on and thinking that their business was going to come back, the retail store was going to come back or someone’s going to come and lease their large big box retail store on a main drag near a mall or in a mall and it didn’t come back like people thought it did. There are some stragglers coming out that are willing to sell these things at pretty good deals.

Certainly in the last 24 months, we’re seeing some of the retail space into like 30,000 a square foot give or take type of box has been hot. It’s like a Ross Dress for Less and like a Michael’s side by side and they’re going in all over the place. TJ Maxx and the other one and they’ve got 10,000, 15,000 square foot concepts and so they’re eating them up.

If you’re getting up into like 80,000, 100,000 square foot big box like that, especially when they’re super deep, there’s just not a whole lot you can do with it. Are we going to put like twenty bowling alleys in there, like one next to the other? It’s hard to lease anything past 75 foot depth in a retail type of environment.

Those are the types of buildings that we want. If I’m going to take the time to build a new asset, I’m going to build an asset that’s institutional nature, which means I need at least 65,000 net rentable square feet. After you count about 25% loss to hallways and offices, bathrooms and mechanical closets, I need to buy spaces that are 80,000 to 100,000 gross square feet to hit that net rentable square foot target that I need to make an asset that is attractive to an institutional buyer that has a cheaper cost of capital.

The interesting thing about that big box retail conversion and even the Class A development strategy, which we’re going to pull that apart much further here, it’s different than a lot of the aggregation play, at least in the deals that I am an owner in for storage. The existing stuff was a little more in the middle of the block, maybe even off of the main beaten path. It’s like, “What the hell do we do with this parcel? We’ll put storage on it.”

It’s starting to transition now more into this I would say it was much more squarely industrial property where that was the location and it was fine. Farmland, like off the beaten path. It’s making the shift more toward this retail type of environment. Look at the facade on the design for the Lawrenceville project that we have.

It’s like way more fancy, way more retail style. It’s on a main strip and it’s got a parking lot and you’re driving by and you’re like, “What is that?” It’s like glass in the in the windows and everything like that. You have this retail structure that’s now being built for the Class A facilities. In the big box retail, clearly that was retail, so that location worked for retail before.

I think that speaks toward that same trend that we touched on a little earlier in the episode, Fernando, where it’s the third or fourth bedroom. If Starbucks is the second place or the third place, it’s like home, work, Starbucks, then this would be the second place for that apartment or the smaller house. Now it has to be like retail located within that same walking distance of the apartment buildings and driving distance of the large apartment buildings. Whereas that really wasn’t how it was done twenty years ago. It’s interesting.

Nowadays, it’s over 65% of the customer base that you’ll have at a given facility. The storage facilities located within or less than ten-minute drive time from either where they work or where they live. Obviously, if you put a storage facility in industrial corridor, no one lives near that. If you put them out in the farmland, maybe some people live there but like not the major populations that you’re trying to go after.

You can’t lease them. What’s the percentage? It’s like 40%, 50% come from someone drove by and saw the sign. Am I far off with that?

No. We’re still a very visually triggered option. People never see self-storage. They’ll drive past six different self-storage facilities and they’ll never even register until the day they need it. They’ll be driving one day and they say, “There’s a facility I can go to.” That’s the largest percentage. The second largest percentage, and we can talk about this too, which shows the importance of bringing self-storage into the 21st century is the second largest percentage of people they find their storage facility by typing in self-storage near whatever city they’re in.

People never see self storage until the day they need it.

Self-storage in Lawrenceville, self-storage in Bucktown, what have you. Whatever search results show up, most likely that’s one of the ones that they’re going to look at and see if it’s on the driving path by clicking on Google maps. If you don’t have a facility that’s online that has a Google business profile that shows up on Google Maps, shows up on the front page of Google, at least in the first three slots, you’re going to be losing a lot of business.

How important is it for that same operator of self-storage to then have a website where you can book right there online, get the credit card in before you even drive over with your pickup truck full of junk? Is that important?

That’s super important. Just like in your business, a seller is the most motivated the second they call you every minute that you have missed that call and you haven’t called them back, their motivation is dropping or they’re already starting to call competitors looking for other options. Have a system that makes it easy. I always think about Apple. In the old days, their whole concept was you need to be able to do everything on your phone within two clicks or less. If I can get somebody to come to my website, find the unit they need, click to reserve and then put in their credit card information, that’s a win.

It speaks to the same thing we were already talking about. It’s like the Amazon effect. We have to have a seller have to call them back right away, but if your toilet is clogged or your water heaters leak, you want that same instantaneous service from the plumber. I don’t know that that was any different 20, 30 years ago as it is now, but those who embrace technology and have the ability to digitize businesses like this are, it’s another trend that’s happening as we speak.

The Big Box Retail And Staying Resilient